The global race for artificial intelligence is no longer just a contest of algorithms, but a struggle for physical infrastructure, massive 300 MW–scale data center clusters that bind together electricity, water, and territorial power. These hyperscale sites are becoming a new axis of geopolitical competition, concentrating capital, reshaping grids, and locking countries into long‑term dependencies on cooling technologies and resource flows. Data centers have become the invisible factories of our daily lives, massive physical infrastructures we never see, yet which support every digital gesture, from a simple HTTPS protocol to the deployment of giant language models executed in parallel. They do not produce material goods but compute billions of floating point operations per second, essential to our economy.

Thermodynamically, their operation rests on a strict equation: they convert almost all electrical energy into heat through the Joule effect, which must be extracted to keep silicon junctions below the critical threshold of 85°C. For households, electricity prices remain visible and politically sensitive, but for digital giants the key variable is industrial power purchase agreements, where raw electron prices can range between 0.06 and 0.10 euros per kilowatt hour. At hyperscale, exploding volumes make the total energy bill colossal, even at these negotiated prices.

However, the reality behind this use is far more complex than official communications suggest. Amazon Web Services recently highlighted a Water Usage Effectiveness (WUE) of 0.12 liters per kilowatt‑hour, compared to its revised global average of 0.19 L/kWh. This figure represents a theoretical optimum, valid only under very favorable climates or ideal operating conditions. As soon as external heat peaks exceed 35°C or high‑density clusters operate at full load, real WUE can easily rise to 1.5 or even 2 L/kWh for evaporative technologies. Meanwhile, average WUE across U.S. data centers is projected to rise toward 0.45–0.48 L/kWh as hyperscale AI clusters proliferate.

This variability depends directly on the different generations of cooling systems coexisting on the global market. First‑generation installations relied heavily on open‑circuit cooling towers, extremely water‑intensive due to direct evaporation. Intermediate generations introduced more sophisticated adiabatic systems, using evaporation only when outdoor temperatures exceed a threshold, thus limiting annual consumption.

Stay ahead of the geopolitical week.

MD Briefing delivers expert analysis across five global fronts — the Indo-Pacific, energy, geoeconomics, European security, and the Middle East — every Monday morning. Free.

The Explosion of Computing Power and the End of Air Cooling

Today, with the rise of artificial intelligence, the electrical power demanded by servers has increased dramatically, from 5 to 10 kW per rack in the past to 40 to more than 100 kW per rack, pushing air cooling to its physical limits. Air can no longer evacuate such heat loads. The sector is therefore shifting to a new technological generation: direct‑to‑chip liquid cooling or immersion of servers in dielectric fluids. These cutting‑edge technologies operate in closed loops and reduce direct water consumption to near zero but require substantial upfront investment. Microsoft has already deployed zero‑water cooling designs using chip‑level liquid cooling, avoiding more than 125 million liters of water per data center per year, although this figure reflects an idealized scenario that is difficult to scale across the fleet, with a fleet‑wide WUE average of 0.30 L/kWh in 2023 showing that most facilities still rely on significant water use despite the headline claims.

Servers Never Rest

AI servers generate extreme heat because they operate continuously and at very high computational intensity, forcing a permanent trade‑off between water footprint and energy footprint, a systemic tension known as the Water‑Energy Nexus. Systems relying on water evaporation can reduce Power Usage Effectiveness (PUE )toward an optimum of 1.1, but at the direct expense of water footprint. Conversely, “dry” systems with large ventilated heat exchangers and mechanical compressors preserve water but increase electricity demand, degrading PUE to 1.4 or 1.5. The 2025 DCA Water Usage Guide stresses that optimizing PUE alone is no longer sufficient, as water dependency has become a critical operational and regulatory risk.

This is precisely why the UN warns that environmental choices focused solely on immediate carbon reduction can worsen the water crisis. In operational reality, a 1‑MW legacy data center using standard evaporative technologies in a warm temperate climate consumes up to 25,500 m³ of water per year, the equivalent of the annual consumption of about one hundred European households. At the scale of today’s 300 MW hyperscale AI campuses, these trade‑offs are no longer engineering optimizations but structural constraints that determine whether a region can physically and politically host such infrastructure.

Giant Open‑Air Radiators and Global Footprints

At the global scale, the water footprint of AI is approaching a critical tipping point. By 2030, AI‑dedicated data centers will consume water equivalent to the basic domestic needs (50–100 L/day) of 1.3 billion people. This explosion is directly linked to the parallel growth in electricity demand, which could reach 945 TWh in 2030. This electricity itself carries a major indirect water footprint, especially in regions where production depends on thermal or nuclear plants requiring 1 to 3 liters of water per kWh for condensation. The expansion of AI infrastructure could result in a net increase of more than 9 trillion liters of water consumption per year by 2030.

The total water footprint therefore extends beyond on‑site cooling: it includes indirect water used for electricity production and the ultra‑pure water required upstream for semiconductor manufacturing, where a single advanced chip‑fabrication plant consumes tens of thousands of cubic meters of water per day. These thermodynamic limits cascade directly into the economics of AI infrastructure.

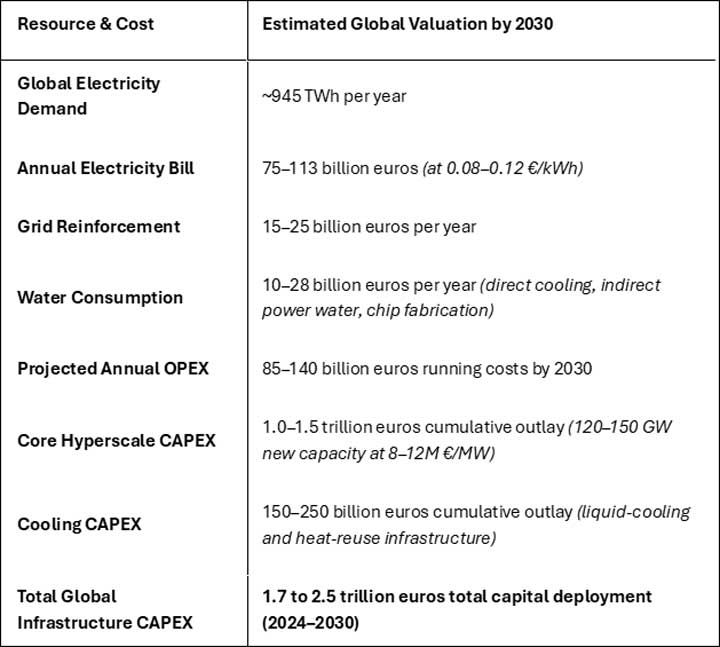

The Macroeconomic Cost of AI Infrastructure to 2030

Behind the thermodynamics lies a second, equally structural constraint: the macroeconomic cost of the AI infrastructure wave. By 2030, the global AI data‑center ecosystem will require three converging cost streams: electricity, water, and capital expenditure for new capacity and cooling technologies, producing a global bill without precedent. These costs converge into three structural streams, electrons, water, and capital, summarized below.

The macroeconomic environment dictates that annual operating costs will escalate to 85–140 billion euros by 2030. This financial burden is highly concentrated rather than evenly distributed across the international system. The United States and China will account for 70–80% of global spending, with the U.S. leading due to its hyperscaler concentration and cheap electricity, representing 40–45% of global cost. China follows with 30–35%, driven by state‑led AI expansion and a water‑intensive, coal‑based electricity system. Europe, constrained by high energy prices and strict regulation, will represent 15–20% of global cost, paying more per MW than any other region, while Russia, isolated from global semiconductor supply chains, will remain marginal at 1–3%. This bipolar distribution accurately mirrors the global semiconductor map, the cloud market, and the energy‑water nexus.

The European Geopolitics of Water and Data Centers

Northern countries such as Finland, Sweden, and the Netherlands benefit from abundant freshwater, regular precipitation, and climates favorable to free cooling, making pressure on freshwater reserves nearly zero. Hyperscalers concentrate infrastructure there to ensure operational and regulatory security ahead of future environmental directives. Within Europe, France occupies a particular position. Its large nuclear fleet provides relatively low‑carbon baseload electricity and, for industrial consumers, long‑term contracts that can approach 0.06–0.08 €/kWh, far below retail tariffs. This nuclear advantage could make France a natural host for energy‑intensive AI clusters, but it collides with growing social and regulatory scrutiny over water withdrawals for both power plants and data centers, especially under recurrent summer heatwaves.

Southern Europe, including Mediterranean France, Spain, Italy, and Greece, faces critical summer water‑stress indices, marked by prolonged droughts and aquifer recharge often below 20%. In these regions, the risk of conflict with agriculture is the most strategic and realistic point in AI development. Agriculture already captures more than 70% of available water for irrigation. The arrival of major industrial infrastructure capable of withdrawing several hundred thousand cubic meters per year creates direct competition for the resource during shortages.

The argument that locating these centers far from cities, in rural areas, solves the problem is false. A large 50‑MW data center using evaporative cooling consumes between 300,000 and 500,000 m³ of water per year. Injecting such demand into a rural distribution node or a local aquifer not calibrated for industry disrupts the hydrological balance of an entire watershed.

In rural areas, water consumed by the system is permanently removed from the immediate terrestrial cycle because it is released as high-temperature vapor into the atmosphere. This localized atmospheric injection creates a thermal plume that elevates localized air temperatures and ambient humidity, preventing regional condensation over the immediate area and shifting precipitation patterns further downwind. Consequently, the local hydrological cycle fails to reset, accelerating the drying of superficial aquifers and directly reducing low-flow river discharge during critical dry seasons.

AI Infrastructure as a New Axis of Global Power

The global race for AI infrastructure is no longer a technological contest but a structural confrontation between the world’s major powers, each constrained by its own endowment of electrons, water, cooling capacity, and semiconductor access. The United States and China alone will account for 70–80% of global AI infrastructure spending by 2030, while Europe, India, and Russia occupy asymmetric but strategically revealing positions.

The United States dominates through scale, cheap electricity, and a mature cloud oligopoly capable of mobilizing 120–150 GW of new AI load. Its advantage rests on vast land availability and industrial PPAs at 0.06–0.10 €/kWh, but it is structurally exposed to water stress, grid congestion, and the vulnerability of long inland gas corridors feeding LNG and power plants. The U.S. leads the AI revolution, yet its thermodynamic foundations are fragile.

China follows with a state‑driven expansion anchored in a coal‑based, water‑intensive electricity system. Severe water scarcity in the North China Plain and semiconductor export controls impose structural constraints, pushing Beijing to accelerate nuclear and hydro deployment and to relocate data centers to cooler northern provinces. China views AI infrastructure not as a market but as a pillar of national power, inseparable from industrial policy and technological sovereignty.

Europe faces the highest structural constraints. High electricity prices, fragmented regulation, and acute water stress in Southern Europe limit its capacity to scale. Northern countries such as Finland and Sweden offer climatic and hydrological advantages, but the continent as a whole risks becoming a consumer rather than a producer of AI capacity unless it develops a coherent strategy for energy, water, and cooling sovereignty. Europe pays more per MW than any other region, a geopolitical handicap in a capital‑intensive race. Beyond the transatlantic and Sino‑American poles, a third actor is reshaping the map.

India emerges as the strategic swing power of the AI resource race. Its electricity demand is growing at one of the fastest rates globally, intersecting with dependence on imported LNG and chronic water scarcity in northern and western regions. Heatwaves regularly exceeding 45°C make evaporative cooling unsustainable, forcing India toward energy‑intensive dry cooling and raising operational costs. Geopolitically, India is constructing a hybrid digital sovereignty model: partnering with U.S. hyperscalers while building domestic semiconductor capacity and securing alternative energy corridors. The India–Middle East–Europe Corridor (IMEC) is central to this strategy, linking India to European markets through a secure, non‑Chinese route for energy, data, and industrial flows. India is not yet a hyperscale superpower, but its demographic scale, strategic flexibility, and corridor diplomacy give it disproportionate influence over the emerging AI order.

Russia, by contrast, combines abundant gas, abundant water, and a cold climate with near‑total isolation from advanced semiconductor supply chains. It can build regional AI capacity for military and state use but cannot compete globally. Its marginal share of global AI infrastructure, spending 1–3%, reflects structural technological isolation rather than resource scarcity.

Territorial Engineering and Digital Sovereignty

A new geopolitical map emerges. AI infrastructure becomes an axis of global power structured not by algorithms alone but by thermodynamic advantage. Nations capable of securing cheap and reliable electrons, resilient water systems, and advanced cooling technologies will shape the digital order of the 2030s. At the scale of 300 MW hyperscale campuses, these advantages or weaknesses become irreversible choices embedded in land, grids, and watersheds. Geopolitical power thus converges with territorial engineering. The ability to dominate AI infrastructure no longer depends solely on macro‑investments or semiconductor access, but on the capacity to reorganize national space around the physical constraints of computation across four axes: where hyperscale clusters are authorized, how scarce water is allocated, which grids are reinforced, and what cooling technologies are mandated. Digital sovereignty will increasingly depend on hydrological sovereignty, in other words, the ability to secure, allocate, and regulate water for computation.

The competition between the United States, China, Europe, India, and Russia is no longer a technological rivalry but a contest over land, water, and the governance of physical infrastructure, the material foundations upon which digital power ultimately rests. Nations that maintain digital sovereignty will be those capable of imposing intelligent territorial planning, demanding full transparency on water withdrawals, and requiring strong technological shifts from operators. This means generalizing closed‑loop systems to approach a WUE of zero, reinjecting extracted heat into district heating networks, and relying exclusively on treated wastewater for residual cooling needs. The future of the digital transition will depend not only on algorithmic power but on the responsible management of this discreet and vital resource that conditions both human life and the resilience of infrastructures.

*This analysis draws on documented assessments by Eurelectric, the IEA, Uptime Institute, McKinsey, and Synergy Research, which together map the geopolitical and cost dynamics of AI infrastructure. Consumption and cost data for European countries are drawn from evidence-based analyses by Eurelectric and the best international network management practices in Portugal, Ireland, and the Netherlands.