Chinese PSCs are state-adjacent actors embedded in China’s overseas economic expansion, particularly under the Belt and Road Initiative (BRI), generating new arenas of US–China security competition in fragile environments.

Existing regulatory frameworks have not significantly constrained this trend. International rules remain fragmented, while domestic regulation has facilitated overseas activity. Demand is driven by BRI exposure in contexts where Chinese capital outpaces host-state security capacity, contributing to PSC proliferation in unstable environments.

The analysis uses Russia’s Wagner Group as a benchmark for escalation dynamics, illustrating how hybrid security actors may shift from commercial cover toward deeper state-linked projection under conditions of strategic reliance.

Structure, Governance, and Expansion Logic

Stay ahead of the geopolitical week.

MD Briefing delivers expert analysis across five global fronts — the Indo-Pacific, energy, geoeconomics, European security, and the Middle East — every Monday morning. Free.

Chinese private security companies have expanded rapidly along BRI routes in the Middle East, North Africa, and sub-Saharan Africa, driven by the need to protect Chinese personnel, assets, and infrastructure in high-risk environments. Their growth reflects rising demand for security around ports, energy facilities, transport networks, and supply chains tied to China’s expanding overseas footprint.

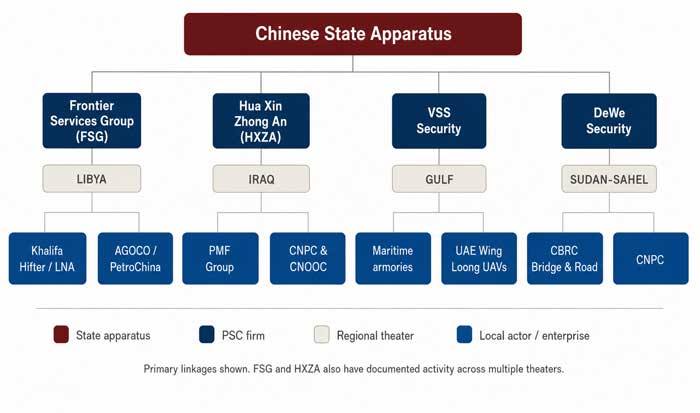

Although formally private, many operate within a state-aligned ecosystem, with regulatory ties, personnel links, and expectations of support for China’s overseas priorities. As a result, the boundary between commercial security provision and state influence is often blurred, with PSCs functioning as extensions of China’s broader external presence. Chinese PSC activity operates within a broader state-linked ecosystem spanning Chinese institutions, enterprises, and local partners. Figure 1 summarizes this structure and the regional scope of analysis.

BRI as Demand Driver

The Belt and Road Initiative, a global infrastructure network spanning over 150 countries, is the primary driver of Chinese PSC expansion. Its scale places Chinese assets and personnel in environments with uneven security provision, generating sustained demand for protection of ports, energy facilities, transport corridors, and supply chains. Chinese PSCs emerged from a loosely regulated domestic sector and were later consolidated under public security oversight, embedding their overseas role within state-aligned structures.

This arrangement is self-reinforcing. State-owned enterprises prefer Chinese PSCs due to cost, familiarity, and policy alignment, while these firms operate within a governance framework that links commercial activity to state strategic objectives. Demand thus drives institutional expansion, which in turn reinforces state adjacency.

BRI projects also generate security externalities. In countries such as Zambia and Pakistan, debt stress and repeated attacks on Chinese personnel and infrastructure have increased demand for convoy protection, evacuation, and risk management services. This creates a feedback loop in which BRI expansion produces insecurity, PSCs absorb risk, and improved security enables further exposure.

Legal and Normative Environment

The international regulatory framework governing PSCs is fragmented and weak. The Additional Protocol I to the Geneva Conventions restricts mercenary protections but relies on narrow definitional thresholds that are difficult to apply in practice. The United Nations’ 1989 Mercenary Convention reinforces these prohibitions but remains limited in effect due to low ratification and weak enforcement.

More recent instruments — the 2008 Montreux Document and the 2013 International Code of Conduct (ICoC) — are the most developed multilateral norms, but both are non-binding. China is a signatory to the Montreux Document, signaling formal alignment with emerging standards. China’s non‑participation in the ICoC is partially offset by the accession or participation of at least one of its larger PSCs, HuaXin ZhongAn (HXZA), which is a founding member of ICoCA and is ICoCA‑certified, and by Sinoguards Marine Security’s participation as a signatory at ICoCA’s 2016 Annual General Meeting, suggesting that reputational incentives for this form of legitimization operate at the firm level as well as at the state level.

Domestic Chinese regulation provides tighter control but also institutional embedding. The 1996 Law on Control of Guns restricts the overseas carriage of weapons, with limited exceptions for maritime operations, shaping the defensive posture of Chinese PSCs. The 2009 Regulation on the Administration of Security and Guarding Services formalized PSC governance under public security oversight, creating a structured but state-linked sector. Unlike commercially independent Western firms, Chinese PSCs are structurally integrated into state oversight while preserving plausible deniability.

Rather than constraining expansion, this fragmented legal and regulatory environment interacts with stronger structural forces on the demand side, most notably China’s overseas economic exposure under the BRI.

Private security companies (PSCs) and private military companies (PMCs) differ in function and purpose. PSCs are primarily defensive and commercial, providing personnel protection, supply chain security, convoy escort, and risk management in environments with limited state capacity.

Chinese PSCs broadly resemble firms such as GardaWorld or Triple Canopy, operating within legal frameworks and coordinating with host governments. PMCs, by contrast, are closer to combat formations used to conduct offensive operations and enable force projection without formal military deployment.

Chinese PSCs should not be equated with Russia’s Wagner Group, which was a state-linked paramilitary actor used for offensive operations under conditions of plausible deniability. Wagner is analytically relevant not as a comparator but as a benchmark for escalation dynamics, illustrating how hybrid security actors can evolve from semi-deniable instruments into more overt paramilitary formations.

This trajectory is used only as a reference point to show how security providers in permissive environments may, under expanding state reliance and strategic pressure, shift along a continuum from commercial protection toward deeper state-linked security projection.

In the Chinese case, PSCs remain primarily commercial and defensive, though their close alignment with state interests means their overseas role cannot be understood purely in private-sector terms as external exposure and expectations evolve.

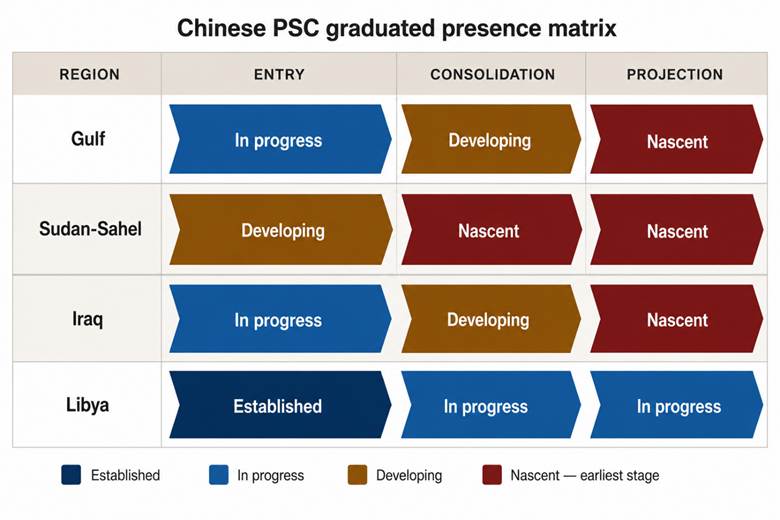

Figure 2 maps the three-stage trajectory of Chinese PSC activity from entry to projection, highlighting increasing operational embeddedness over time.

Stage 1 (Entry) refers to the initial phase of overseas deployment, where security actors establish a foothold through low-visibility, limited-scope roles that are framed as advisory or protective rather than operational or coercive. Wagner’s 2014 deployment in Ukraine exemplifies this. Initial operations in Crimea and later Donbas embedded alongside regular forces under a deniable advisory guise, masking what was effectively state intervention.

In the Central African Republic, the same operational logic operated through a different entry pathway, illustrating the framework’s flexibility. Russian diplomatic re-engagement enabled a 2018 security agreement under which Wagner-linked “instructors” deployed near strategic resource zones, exploiting gaps in local security capacity and laying the groundwork for foothold consolidation and dependency formation.

Syria deserves mention as an important theater of Stage 1 operations. From 2015, Wagner deployed in an advisory and force-protection capacity in support of Bashar al-Assad’s forces. The Syria mission functioned as both a combat proving ground and a logistical bridge to subsequent African operations, including the Libyan airbridge later documented by UN investigators. The February 2018 attack near Deir ez-Zor, in which Wagner-linked personnel suffered heavy casualties at the hands of the US military, illustrates the escalatory risks embedded in ostensibly advisory deployments.

Libya followed a similar pattern but escalated more rapidly. Wagner personnel initially embedded in advisory roles with warlord Khalifa Hifter’s forces in 2018 but quickly shifted into direct operational activity, including control of airbases and deployment of systems such as Pantsir-S1 air-defense batteries.This underscores how entry conditions can accelerate in fragmented environments where strategic assets are contested.

Stage 2 (Consolidation) marks the transition from presence to embedded control. At this stage, the PMC secures formalized protection arrangements with host actors, acquires sustained access to strategic economic assets, and becomes structurally integrated into local security and political economies.

In the Central African Republic, Wagner entrenched a dependency relationship with the host state so deeply that it operated above regime turnover, becoming the dominant security intermediary through which external actors engaged the country.

In Libya, consolidation involved co-opting Libyan-owned assets and narrowing operational focus. During the Tripoli campaign, Wagner divested Saudi partners and shifted to a single-theater operation, while its deployment of Su-35 fighters signaled a refocus on control rather than commercial security provision.

Stage 3 (Projection) represents the weaponization of accumulated presence as geopolitical leverage. Wagner reached this stage in Libya around 2020. Notably, the group’s presence in the Sharara oilfield, sustained through armed convoys, translated into influence over Libyan energy production beyond a conventional contractor role.

Moreover, Wagner’s control of the Qardabiyah, Jufra, and al-Khadim airbases enabled an airbridge from Syria to the Sahel and sub-Saharan Africa, documented across 338 cargo flights originating in Syria and transiting Libya. Finally, political influence operations, including messaging in support of Saif al-Islam Gaddafi and Hifter-aligned narratives, illustrate projection as political engineering designed to shape Libya’s internal balance regardless of formal authority.

Although differences still outweigh similarities, Chinese PSCs have undergone their own evolution, and further development could, in principle, move in a more Wagner-like direction. Beijing may view such a shift as a potential shortcut to strengthening power-projection capabilities in the Middle East —a gap repeatedly exposed since 7 October 2023, when China’s limited ability to deploy military force left it unable to protect or advance its interests amid widespread regional conflict.

Chinese PSC Entrenchment Across MENA: A Comparative Analysis

Each of the four Chinese PSC case studies examined below map onto different points along the Wagner-style trajectory: the Gulf States (entry), the Sudan-Sahel corridor (consolidation in progress), Iraq (consolidation), and Libya (consolidation-projection transition). Together, they illustrate how Chinese PSCs evolve from bounded commercial presence toward deeper strategic positioning. Across all four cases, commercial framing functions as an evidentiary shield, complicating attribution while masking state-aligned activity behind ostensibly private actors.

The Gulf States (Entry)

The Gulf states — primarily the United Arab Emirates and Saudi Arabia — illustrate the entry and relationship-building stage for Chinese security firms, forming the lower anchor of the trajectory. Capable regional militaries and the likely US response to a larger Chinese footprint constrain Chinese PSC ground-level engagement. HXZA operates across the Gulf of Aden, Gulf of Guinea, and parts of Africa, the Middle East, and South Asia, providing maritime and international security services. Disruptions in the Red Sea and wider regional tensions create incentives and openings for expanded Chinese PSC maritime security activity.

However, there is no open-source evidence that HXZA — or other Chinese PSCs — has conducted Red Sea patrols or armed escort missions comparable to Western private maritime security firms. This absence suggests their role remains primarily land-based and commercially oriented rather than focused on high-risk maritime operations.

HXZA presents itself as a “privately held” maritime security and risk-management firm, but is closely tied to the Chinese state: founded by a former PLA officer, licensed and regulated by Chinese authorities, staffed by former military personnel, and primarily serving state-owned enterprises. Such positioning is less important for its factual content than for what it signals about client-facing strategy. By emphasizing independence and technical capacity, firms like HXZA build credibility and relationships that may enable deeper future engagement, even as their current operational footprint remains limited.

Overall, engagement remains commercially bounded, but the relationships formed at this stage create a latent foundation for more expansive roles under shifting regional security conditions.

The Sudan-Sahel Corridor (Entry-Consolidation)

The Sudan–Sahel corridor provides a useful case for assessing how Chinese private security activity may evolve in practice. The partial withdrawal of Russian PMCs from parts of Africa has opened space in some environments where alternative providers could, in principle, expand. However, any such shift remains uneven and context-dependent, constrained by legal limits on Chinese personnel carrying weapons and limited evidence of sustained operational deployment.

Available cases are best understood as isolated precedents rather than evidence of systemic entry. For example, China United Safety Technology (Tianjin) Group (VSS) was involved in the 2012 rescue of 14 Chinese workers kidnapped in South Kordofan, Sudan, reportedly in coordination with local actors. Similarly, DeWe Security participated in the evacuation of more than 300 Chinese oil workers in South Sudan during periods of acute insecurity.

These incidents are better interpreted as ad hoc crisis-response operations rather than sustained security provision. At most, they suggest that Chinese firms have developed limited experience operating in coordination with local security environments under exceptional circumstances, rather than a consistent pattern of embedded or partner-enabled deployment.

Iraq (Consolidation)

Iraq provides the clearest example of consolidation. Chinese PSCs operate under infrastructure protection mandates for multi-billion dollar China National Petroleum Corporation (CNPC) and China National Offshore Oil Corporation (CNOOC) energy projects within a layered security structure involving Iraqi forces, local police, and Chinese personnel responsible for inner perimeter security.

The 2014 evacuation of over a thousand Chinese workers during the Islamic State (Daesh or ISIS) siege of Samarra further indicates that Chinese PSCs had moved beyond static guarding into active operational response, a key marker of consolidation even within a commercially framed context.

The arrangement is not purely passive. Experienced Chinese PSCs supporting oil and gas operations in Iraq rely in part on established ties with Iraqi Popular Mobilization Forces (PMF), particularly where coordination with Baghdad is limited. This reflects a broader pattern of engagement with sub-state actors seen as more capable of securing operational environments, also evident in Afghanistan (pre-2021 contacts with the Taliban) and Myanmar (cooperation with ethnic armed groups along infrastructure corridors).

While some PMF factions have attacked US personnel in Iraq and Syria, there is no clear evidence that Chinese PSC engagement has directly increased their lethality. However, limited indicators — such as logistics access, site security practices, and operational proximity — suggest potential pathways for informal capability diffusion. Even without deliberate force enhancement, this creates a structural interface between Chinese-guarded assets and militia-linked actors, introducing a marginal but non-trivial risk channel for US forces operating in the region.

Libya (Consolidation-Projection Transition)

Political fragmentation between Tripoli and Khalifa Hifter’s Libyan National Army (LNA), alongside an ineffectively enforced UN arms embargo, has enabled engagement with sub-state actors.

The Libya timeline broadly aligns with the three-stage framework. Entry involved Frontier Services Group (FSG), which proposed integrated security packages spanning ISR, UAVs, maritime interdiction, and related capabilities. FSG — founded by Erik Prince but backed by Chinese capital and training infrastructure in Beijing — represents a hybrid entity that nonetheless reflects a wider pattern of commercially framed entry followed by potential operational deepening.

Consolidation has been associated with reported engagement with Hifter, including claims involving FSG-linked logistics and training arrangements and UAE-connected support initiatives. However, the evidentiary base is limited and does not demonstrate a consistent or repeatable pattern; at most, it loosely parallels Wagner-style consolidation through incremental deepening of ties around a partner force.

More concretely, China’s presence in Libya reflects renewed commercial re-engagement, including PetroChina’s reported 2018 agreement with the National Oil Corporation for an annual crude purchase contract, its first since 2013. This signals a return to upstream energy activity rather than any shift in security posture.

Chinese PSCs currently play a limited and indirect role in Libya’s fragmented security environment. Unlike Russia, China has not developed a consistent pattern of using private security actors for external force projection, and there is little evidence of movement in that direction.

Separately, reported use of Chinese-made Wing Loong II UAVs via commercial or third-party channels highlights dual-use supply chains linking Chinese defense production to conflict environments. However, this reflects arms proliferation dynamics rather than the deployment of Chinese security personnel.

Overall, Libya remains an illustrative but not decisive case: China’s engagement is still primarily commercial and energy-focused, with only indirect exposure to local security dynamics and no clear transition toward security projection.

Implications: Strategic Competition and the Governance of Security Provision

Chinese PSCs link overseas economic expansion with security provision in fragile environments. Viewed through a Wagner lens, they may show limited functional convergence, where commercial activity can become embedded and generate strategic effects.

This contributes to a gradual expansion of Chinese influence that may indirectly affect U.S. personnel and infrastructure abroad and reflects the diffusion of US–China competition into the security domain.

Current conflict dynamics in the 2026 Iran war show that Gulf infrastructure is directly exposed to spillover, with Iranian strikes and threats disrupting energy sites, shipping, and other critical assets across neighboring states. At the same time, regional security and investment patterns are becoming more flexible and issue-driven, creating openings for adaptable non-Western actors.

Chinese PSCs typically enter new regions through limited commercial functions such as maritime escort, supply chain protection, and infrastructure security. In the Gulf, firms such as HXZA illustrate this entry stage, building credibility while remaining constrained by capable host-state security services and the political costs of visibility.

Some PSCs then become embedded in protecting Chinese overseas investments, particularly within Belt and Road corridors where capital exposure intersects with instability. This consolidation involves sustained infrastructure protection and proximity to state and sub-state actors. In Iraq, PSC activity overlaps with Popular Mobilization Forces, including factions hostile to U.S. forces.

In a more advanced projection phase, PSCs may integrate further into strategic infrastructure ecosystems spanning transport, energy, and logistics. The Libya case suggests sustained economic-security entanglement can generate indirect influence over connectivity and resource flows without military deployment.

These dynamics are reinforced by fragmented global governance frameworks: regulation is weak, enforcement limited, and cross-border oversight minimal.

Chinese PSCs should therefore be neither overstated nor dismissed. They are neither extensions of Chinese military power nor neutral commercial actors, but contingent instruments shaped by host-state conditions and contractual environments.

John Calabrese teaches international relations at America University and is non-resident Senior Fellow at the Middle East Institute and book review editor for The Middle East Journal.

This analysis benefited substantially from the work of the Boston Risk Group, a student-led research organization at Tufts University. The author is especially grateful to Sam C. Weinstein (Research Head), Finnigan Barret, Sabina Cherner, Caleb Epstein, Evan Krauthiemer, Natasha Roseman, and Daniel Figueroa (Editor) for their research assistance, source identification, fact-checking, and analytical support throughout the project.

Thanks to Ken Pollack, Alistair Taylor, and Czekaj of the Middle East Institute for their comments and suggestions.