In the space of ten days, President Xi Jinping received the two leaders most capable of reshaping the global economic order. President Donald Trump left Beijing trailing vague promises of agricultural purchases and no binding commitments. [1]

President

Vladimir Putin arrived with something more durable: a partnership defined not by paperwork but by mutual strategic necessity. [2]

While Beijing choreographed summits that will shape the architecture of global trade for years, EU commissioners were finalising a set of defensive trade instruments designed, above all, to slow the tide of Chinese goods flooding European markets. The optics are uncomfortable. China is playing offence. Europe is playing goalkeeper. But here is the harder truth that Brussels has yet to say aloud: the problem is not primarily China. The problem is Europe. China has not trapped the continent. Europe has trapped itself – and no overcapacity instrument, however well-designed, will change that until European policymakers are honest about the distinction.

Stay ahead of the geopolitical week.

MD Briefing delivers expert analysis across five global fronts — the Indo-Pacific, energy, geoeconomics, European security, and the Middle East — every Monday morning. Free.

The Numbers and What They Obscure

When the college of commissioners meets on 29 May 2026, the centrepiece of the agenda will be an “overcapacity instrument” – a mechanism that would allow the EU to impose sector-wide caps on Chinese imports where subsidised overproduction is deemed to undercut European competitors. [3]

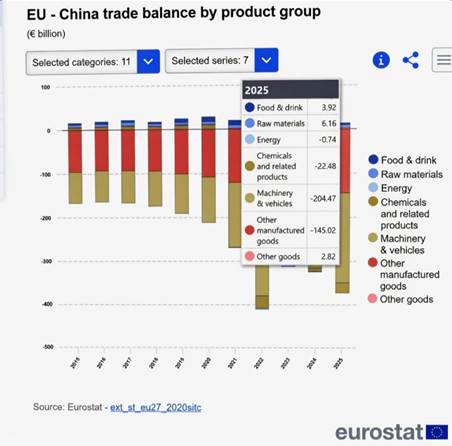

The commission’s case is arithmetically hard to dismiss. The EU trade in goods deficit with China was €360 billion in 2025.

Between January and April this year, Beijing’s trade surplus with the EU reached $113bn – up from $91bn over the same period last year, and accelerating.[4] Steel, electric vehicles, solar panels: in each sector the pattern is the same. Chinese state financing underwrites production at a scale and cost that European firms, operating without equivalent state support, structurally cannot match.

But a trade deficit is a flow. What Europe is actually confronting is a structural condition – an industrial dependency built across two decades of procurement decisions that prioritised cost over strategic risk. China did not create that dependency. European governments and firms chose the cheapest, most efficient global suppliers across two decades of unchallenged growth. China was, for most of that period, a rational answer to a procurement question. The problem is that Europe has no coherent answer now.

Three Summits and a Single Message

To understand why Brussels’ timing matters, it helps to read the President Xi diplomatic calendar not as coincidence but as composition. The President Trump meeting produced the appearance of concession – a softened tariff tone, promises of agricultural purchases – while leaving the structural features of Chinese industrial strategy entirely intact.

President

Xi demonstrated that Washington’s maximalist opening position could be walked back with a bilateral gesture and a photo opportunity. The terms of any genuine rebalancing remain unresolved. The meeting with President Putin served a different purpose. Russia’s value to Beijing is not primarily economic. What Moscow provides is strategic insulation: a partner equally committed to contesting the Western-led order, and a continental relationship that complicates any attempt to apply coordinated pressure on China’s periphery.

Together, the two summits delivered a message with direct relevance to Brussels: China is not isolated, it retains the strategic flexibility to absorb European trade measures without existential discomfort, and it has spent the past ten days demonstrating exactly that. Europe, by contrast, does not have equivalent flexibility. Beijing knows it. And it knows why.

The Paralysis That Precedes China

Europe’s vulnerability did not begin with Chinese overcapacity. It began with a governance architecture designed for market integration, not strategic competition – one that produces a specific and now costly pathology: the ability to diagnose problems with considerable sophistication, combined with a structural incapacity to act on the diagnosis. The record is consistent. The 2019 strategic autonomy agenda identified the dependencies. The 2021 Chips Act acknowledged the semiconductor gap. The 2022 Critical Raw Materials Act named the mineral vulnerabilities. The 2023 Net-Zero Industry Act gestured toward the clean technology deficit. Each initiative was real. Each was underfunded, under-coordinated, and in most cases outpaced by the very trends it was designed to address. European institutions produce some of the most sophisticated geopolitical thinking in the world. It is a failure of conversion – the chronic inability to translate diagnosis into durable, adequately resourced, politically sustained action.

The reason is structural. Industrial policy at European scale requires either a genuine transfer of fiscal authority to Brussels – which member states will not accept – or deep voluntary coordination between governments with fundamentally different economic models. Germany’s export-driven industrialism, France’s statist sovereignty logic, and southern Europe’s investment-hungry growth model are not political differences that can be managed at the margins. They are different theories of economic life, and they pull in opposite directions whenever a genuinely costly strategic choice must be made.

The Germany Problem Is Not Germany

The standard critique points at Berlin. Germany’s structural dependence on Chinese markets and supply chains, the argument goes, functions as a permanent internal veto on European strategic ambition.

That critique is accurate but incomplete. Germany’s hesitation is not obstruction for its own sake. It is a rational response to a genuine structural condition: an economy whose postwar growth model was built on open global markets, high-value manufacturing exports, and reliable low-cost inputs. Asking Germany to embrace economic confrontation with China without a credible alternative industrial framework is not a geopolitical ask. It is an existential one.

The question European policymakers should be asking is not “how do we overcome German resistance?” It is “what would need to be true for Germany – and firms like it across the continent – to accept the costs of strategic reorientation?” The answer requires a European industrial compact that does not yet exist: shared risk, shared investment, shared market access, and shared adjustment mechanisms for the sectors that bear disproportionate transition costs. Without that compact, demanding strategic boldness from member states with the most to lose is not policy. It is a wish.

What De-Risking Actually Demands

The word Brussels has settled on – “de-risking” – deserves scrutiny. It implies a manageable adjustment: shaving exposure at the margins, diversifying selected supply chains, building targeted domestic capacity. It is language calibrated to hold together a coalition of twenty-seven member states without triggering the political costs that genuine strategic reorientation would impose.

The problem is that Europe’s dependency on China is foundational. The continent’s green transition – its most ambitious industrial transformation – is critically reliant on Chinese-controlled battery materials, rare earth processing, and solar panel components. The more urgently Europe pursues decarbonisation, the deeper its exposure to Chinese supply chains becomes. This is a design flaw baked into the transition by a decade of procurement decisions that regulators are now trying to undo with instruments that operate far too slowly to matter.

Genuine de-risking requires three things that European institutions have consistently failed to deliver at the necessary scale.

The first is fiscal firepower: supply-chain diversification and domestic semiconductor ecosystems are not built by regulation, they are built by capital, and the Inflation Reduction Act was above all an investment decision that Europe has yet to replicate. The second is institutional coherence: strategic industrial policy cannot function when it must be negotiated clause by clause across twenty-seven governments and multiple Council configurations.

The third is political honesty: de-risking will impose real costs on consumers, firms, and specific member state economies, and European leaders have not made that case publicly or prepared their publics for what the transition requires.

Speed of legislation is the appearance of strategy.

The Stirrings of Strategic Agency

Europe is not, however, standing entirely still. The Carbon Border Adjustment Mechanism, the Industrial Accelerator Act, and a new steel safeguard framework represent a meaningful, if overdue, shift in the EU’s industrial posture – from passive rule-setter to active strategic actor. Taken together, they signal that Brussels has begun to accept a proposition it resisted for years: that open markets and strategic vulnerability are not the same thing, and that industrial policy is not protectionism by another name.

Spain’s position within this emerging framework is worth watching. Madrid is shaping it toward a specific logic. On the Industrial Accelerator Act, Spain has advanced a “Value in Europe” principle: the argument that preferential treatment should follow genuine industrial contribution, not merely legal registration on European soil. It is a direct challenge to the kind of regulatory arbitrage that has allowed firms to claim European credentials while anchoring their actual production capacity elsewhere.[5]

The principle is straightforward: if Europe is investing public resources to build strategic industrial capacity, the returns – the jobs, the supply chains, the technological capabilities – should be rooted in Europe. Not outsourced through a subsidiary, not offshored behind a compliance label. That is not a protectionist argument. It is a definition of what industrial sovereignty actually requires. Friday’s commissioners’ meeting will produce a decision. It may well be the right one – the overcapacity instrument is a legitimate and overdue tool.

If Brussels treats every new trade defence instrument as a complete China strategy -rather than as one small piece of a broader industrial and geopolitical doctrine that still needs to be built – the imbalance between the European Union and China will only grow deeper. What matters is not the existence of tools, but the absence of a coherent system behind them. The European Union risks confusing administrative competence with genuine strategic capacity: mistaking tariffs for direction, safeguards for coherence, and reaction for design. China, by contrast, operates on an entirely different plane. Its industrial policy, state capital, national champions and geopolitical objectives are fused into one integrated architecture of power. From this vantage point, Europe is being out-composed as a system.

This is why Xi Jinping’s recent diplomatic sequence in Beijing was revealing less for what was said than for what was left unsaid. Over ten days of high-level summits, Europe barely registered as a strategic reference point – meriting neither attention, reassurance, nor even rhetorical acknowledgement.

Brussels may be tempted to read this absence as neutrality. In geopolitics, silence is rarely empty, it signals something more sobering: Europe is no longer central enough in China’s strategic calculus to require explicit articulation.

Europe Confronts the Limits of Openness

Across Brussels and several EU capitals, a more insistent tone is emerging in the debate on Europe’s industrial exposure to China.

The EU’s industry leadership has cautioned that European firms have not sufficiently reduced their strategic dependencies, particularly in relation to China – an assessment attributed in multiple reports to Commissioner Stéphane Séjourné. While reaffirming that openness to trade remains a foundational European principle, he has also pointed to the scale of the imbalance now structuring the relationship, with the EU facing a trade deficit with China estimated at over €360 billion.

What is shifting is not the diagnosis, but the language used to describe it. In parts of the debate, openness is no longer framed as an unconditional virtue, but as something that requires recalibration in the face of asymmetric industrial realities.

That shift is most visible in more politically charged interventions, including from France’s Minister for Foreign Trade Laurent Saint-Martin, who has warned that China stands to gain little from policies that weaken European industry, and has called for a firmer European stance against what he describes as strategic complacency in trade policy.

Alongside this more assertive framing, other voices continue to emphasise balance rather than rupture. Ireland’s Foreign Minister Helen McEntee has underlined that China remains an important economic partner, while stressing the need for greater equilibrium in the overall relationship.

According to multiple reports, these tensions are expected to resurface at the forthcoming European Council summit in June, where leaders are likely to revisit the broader question of how to reconcile economic openness with industrial resilience.

What is emerging, gradually but unmistakably, is a European conversation that is moving away from the assumption that openness alone is a strategy – and toward the more uncomfortable question of what balance now actually requires.

[1] BBC News, coverage of the Trump–Xi Beijing meetings (May 2026), reporting limited agreements beyond agricultural commitments and broader diplomatic signalling.

[2] At their Moscow summit, Xi Jinping and Vladimir Putin extended their Treaty of Good-Neighbourliness and signed a package of bilateral documents spanning energy, trade, technology, and global governance. For Europe, the implication is direct. China is not a neutral economic actor whose trade policies can be addressed in isolation. CNN, reporting on Vladimir Putin’s Beijing visit and the development of Sino-Russian strategic coordination (May 2026).

[3] EUobserver, reporting on the European Commission’s planned discussion of a proposed “overcapacity instrument” at the College of Commissioners meeting of 29 May 2026. Benjamin Fox – “EU-China trade war edges closer as Brussels lines up emergency import safeguards”, 25 May 2026 in EUobserver

[4] Alicia García-Herrero, “Europe’s trade problem with China is becoming more measurable

30 April 2026, available at: https://www.bruegel.org/newsletter/europes-trade-problem-china-becoming-more-measurable

[5] ANSA, “Madrid precisa: ‘Nessuna adesione formale al testo sulla difesa commerciale Ue'” (“Madrid clarifies: ‘No formal adherence to the EU trade defence text'”), 25 May 2026. Madrid clarifies: “No formal adherence to the EU trade defense text.”