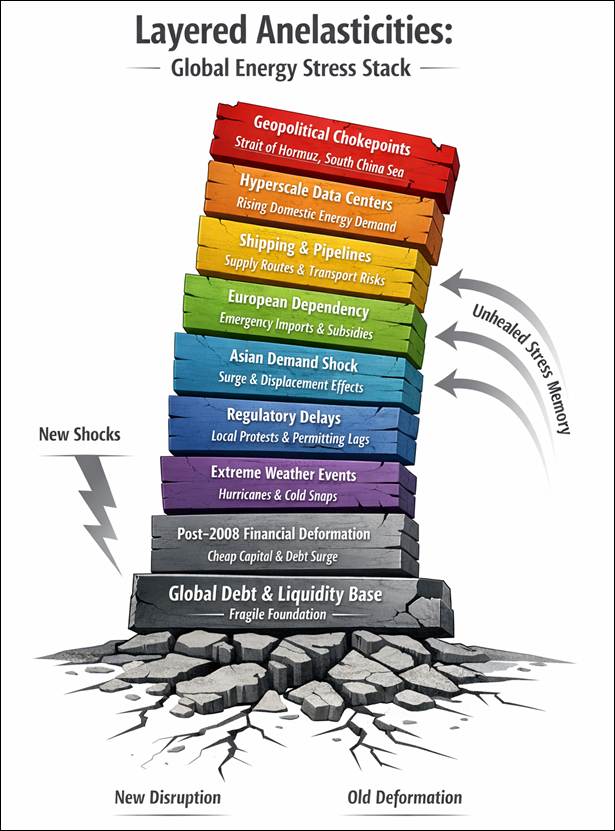

The global energy system increasingly behaves like a material under continuous deformation; anelasticity is the incomplete recovery after stress, while hysteresis is the persistence of that stress in shaping future reactions. The system absorbs shocks, adjusts to new pressures, and yet never fully returns to its previous state. What distinguishes the current moment in energy is the accelerating tempo of events: new disruptions arrive before the system has healed from earlier ones, creating layers of residual tension that accumulate over time. Each disturbance lands on a structure already carrying the memory of previous stress, and that memory becomes part of the system’s architecture.

The Lego‑tower metaphor captures this dynamic. New cubes are added faster than older ones can be reinforced or removed. These cubes represent new technologies, new geopolitical rivalries, new supply routes, emergency interventions, and expanding financial obligations. They accumulate at the top of the structure while the base remains comparatively weak. That base is the global debt architecture spanning the United States, Europe, China, and emerging economies. Debt expands faster than economic capacity; the tower rises faster than its foundation can support, and the system loses its ability to heal.

The Post‑2008 Financial Deformation

The fragility of the global energy system cannot be understood without the permanent deformation left by the 2008 crisis. That episode did not simply trigger a recession; it rewired the financial foundations on which modern energy security rests. Massive liquidity injections, expanding fiscal deficits, and an unprecedented surge in global debt created a new equilibrium in which stability, investment, and even geopolitical risk management became dependent on cheap capital. The system never returned to its pre‑2008 shape. Debt became the silent base of the global tower, able to support growth during calm periods but amplifying instability when shocks accumulate. Every new disruption now lands on a structure already carrying the residual deformation of that crisis, the financial equivalent of anelasticity: the system bent under stress and never fully recovered.

Stay ahead of the geopolitical week.

MD Briefing delivers expert analysis across five global fronts — the Indo-Pacific, energy, geoeconomics, European security, and the Middle East — every Monday morning. Free.

Hormuz and the Persistence of Geopolitical Memory

The Strait of Hormuz is the clearest expression of geopolitical hysteresis: a narrow corridor where the interests of the United States, China, Russia, Iran, Saudi Arabia, the Emirates, and Qatar intersect and collide. It is not only a contemporary chokepoint but a layered historical structure shaped by repeated episodes of coercion, blockade, and militarization.

The Portuguese seizure of 1507, the British blockade during the Mossadegh crisis, the territorial sea extensions of the 1970s, the Tanker War, the 1988 clashes, Iran’s closure threats in the 2000s, and the 2026 war each left a deformation that was never removed. Together they created a price‑formation mechanism that remembers every shock.

The distortions of 2021–2022 further deepen the strategic weight of Hormuz. The European gas crisis tightened global LNG markets, lengthened shipping routes, raised insurance costs, and eliminated spare capacity. Because these pressures never fully unwound, any disturbance at Hormuz now lands on a system already operating under residual strain. A drone incident, a brief naval standoff, or a temporary embargo threat now interacts with the unhealed distortions of 2021–2022, amplifying price reactions and shipping disruptions. Hormuz becomes more destabilizing not in isolation but because it sits atop the unresolved tightness created by the European crisis. As a result, even minor incidents reset insurance costs upward and reroute tankers for months. The system never returns to its previous state; every new event lands on a structure carrying five centuries of accumulated stress, and the memory becomes part of the market itself.

The Middle Eastern Industrial Race

A second layer of competition unfolds within the Middle East itself, it concerns who will supply the first large‑scale ammonia, urea, hydrogen, and the associated logistics chains. Gulf producers seek to position themselves as indispensable partners for Asia and Europe, Iran seeks to monetize its resource base and its geography, these rivalries shape investment flows, diplomatic alignments, and long‑term infrastructure choices.

Here too, new cubes are added before the previous ones have stabilized, capital is committed long before political risk declines, infrastructure is planned before maritime security improves, export strategies are defined before demand certainty exists, the system absorbs the shock of transformation but does not recover quickly, the tower grows taller, but the base does not strengthen proportionally.

The Long Spine of US LNG

The United States adds another dimension through its expanding LNG role, gas must travel long distances from inland basins to liquefaction plants on the Gulf and Atlantic coasts. These routes cross multiple jurisdictions and constraints, forming a continuous chain of potential interruptions, weather, accidents, regulatory decisions, or local opposition can disrupt flows at any point. At the same time, the explosive rise of domestic energy demand from hyperscale data centers intensifies internal gas competition, tightening the system even before exports are considered.

This creates a structural contrast with Qatar and Iran, where extraction sites lie only eighty to one hundred kilometers from export terminals, the difference in exposure is profound. A hurricane in the Gulf can strike before the system has recovered from a regulatory delay in Pennsylvania, a local protest in Louisiana can compound the effects of a pipeline rupture in Texas, a cold snap in the Midwest can tighten supply before maintenance backlogs are cleared, each new event retards the healing of the previous one, and the deformation becomes cumulative.

Asia as the Demand Anchor

China, India, Japan, and South Korea absorb the bulk of global LNG and oil flows, their procurement strategies, storage policies, and long‑term contracts shape global price formation and shipping patterns. When Asian buyers accelerate purchases, markets tighten instantly, when they pause, prices collapse, this behaviour adds another layer of path dependency. When China increases LNG procurement after a cold winter, the system has not yet healed from Japan’s earlier surge, prices spike, shipping tightens, Europe is displaced, the previous distortion becomes permanent.

Europe as a Dependent Actor

The European Union remains largely a spectator in this architecture, it depends on external suppliers, external shipping routes, external security guarantees, and external investment cycles. It reacts to shocks rather than shaping them, its fragmented energy governance and limited upstream leverage reduce its ability to influence outcomes, emergency subsidies, emergency LNG procurement, and emergency storage mandates solve immediate problems but deepen long‑term dependency, they add height to the tower without reinforcing the foundation.

The Crisis Threshold

A short disruption lasting two or three months can be absorbed. Storage can be rebuilt, supply chains can adjust, markets can reprice risk, and even geopolitical tensions can stabilize once actors recognize the cost of escalation. The global energy architecture has repeatedly shown that it can reorganize itself under pressure. The risk emerges only when a crisis pushes into a fourth month without relief. At that point, accumulated stress begins to interact with deeper structural weaknesses: storage depletion, refinery saturation, shipping congestion, liquidity tightening, and sovereign‑risk repricing converge. This is also the moment when the struggle for dominance over energy routes becomes decisive. States begin to test chokepoints, redirect flows, weaponize transit rights, and compete for control of the corridors that determine who absorbs the shock and who exports it. Once these pressures align, the tower built on a fragile global debt foundation becomes vulnerable to a sudden shift. And once it tilts, it does not straighten again.