In the BRICS Summit, a key item in the agenda was the further development of new and complementary reserve currencies and settlement mechanisms. The global economy is slowly moving toward a post-US dollar era.

At the end of March, deputy chairman of Russia’s State Duma Alexander Babakov mentioned that the BRICS countries were working on creating a new trade currency. Babakov expected the BRICS to present ideas on its development at the group’s August summit in South Africa.

Interestingly, a marginal comment was quickly inflated into magnificent disproportions in the West. In reality, the group seeks to foster greater prosperity through diversified development.

From top-down to bottom-up network effects

Stay ahead of the geopolitical week.

MD Briefing delivers expert analysis across five global fronts — the Indo-Pacific, energy, geoeconomics, European security, and the Middle East — every Monday morning. Free.

Ever since then, some international observers from the Wall Street Journal to the Financial Times have derided the idea of BRICS currencies, which is reframed as “de-dollarization.” A BRICS currency, they warn, could shake the predominance of the US dollar, which they see as a nightmare of sorts.

In May – oddly, amid the US banking crisis – economist Paul Krugman attributed the “de-dollarization” brouhaha to crypto-cultists and Putin’s sympathizers, as if the trend was nothing but a misguided anti-patriotic melee. And just days ago, even the ex-Goldman Sachs economist Jim O’Neill, who coined the BRIC acronym two decades ago, dismissed as “ridiculous” the notion that emerging nations might develop their own currency.

In reality, the migration from the US dollar has already started. But it seeks to avoid disruption and does not rely on the kind of top-down network effects, which the US dollar and its precursor the UK pound once used, typically through geopolitics and military might.

Instead, the BRICS promote bottom-up network effects. As the group’s summits suggest, the first step is the transition to settlements in local currencies, to avoid redundant currency intermediaries and foreign-exchange traps. The next step is the establishment of digital currency.

The launch of a potential common currency is still another possible mechanism, but more likely in the long-run.

Bottom-up diversification, sovereign choices

Last spring, Brazil’s president Luiz Inàcio Lula da Silva said he asks himself “every night, why all countries have to base their trade on the dollar.” It is a valid point. Global currency arrangements shouldn’t reflect just the interests of Americans who account for only 4.1 percent of the world population.

Thanks to its organizational flexibility, the BRICS makes possible unilateral, bilateral and multilateral measures. These range from gradual reforms to more unilateral individual measures, which are driven mainly by the original BRICS founder economies (Brazil, Russia, India, China, and South Africa). These measures are also promoted by the new aspiring members and coalition partners who share the BRICS vision and are considering its membership.

Reportedly, some 22 countries have formally applied to join the group, while an equal number of states have been informally asking about becoming BRICS members. Countries looking to join the bloc include Saudi Arabia, Iran, the United Arab Emirates, Argentina, Indonesia, Egypt and Ethiopia. After the 1955 Bandung Conference, the non-aligned countries were organized into a political movement. Today, the BRICS group is building an economic bloc.

Figure 1 Non-Aligned Movement and the BRICS Group

Source: Wikimedia Commons

It is the rising number of large and populous emerging economies that make possible the kind of bottom-up network effects, which will be critical to launch the new infrastructure for the proposed complementary settlement mechanisms. These bottom-up effects are based on choices by sovereign states. By contrast, the dollar-predominance is imposed on the rest of the world, which excludes sovereign choices.

Like asset managers who seek to maintain appropriate diversification in their portfolios, the BRICS’ strategic objective is to recalibrate reserve currencies.

In the multipolar world economy, global growth prospects are driven by the emerging economies; not by the West any longer.

Figure 2 Emerging economies drive global growth, not the West

Source: IMF, May 2023

Exorbitant risks of dollar monopoly

Paradoxically, misguided US policies have accelerated the erosion of the dollar-based regime following the West’s financial crisis in 2008, excessive debt-taking, trade protectionism and technology friction, pandemic-induced depression, and the new Cold Wars.

When the dollar is weaponized by US foreign policy in the name of international community but without the broad support of international consensus, it puts trade invoicing and settlement, foreign corporates, financials and central bank reserves at risk. Hence, too, the recent warning by Fitch Ratings that it may be forced to downgrade dozens of US banks, even the likes of JP Morgan Chase.

After the spring failures of Silicon Valley Bank, Signature Bank, First Republic and the takeover of Credit Suisse by UBS, 200 more banks may be vulnerable to the type of risk that caused SVB to collapse. Across the US, 2,315 banks – almost half of the total – sit on assets worth less than their liabilities.

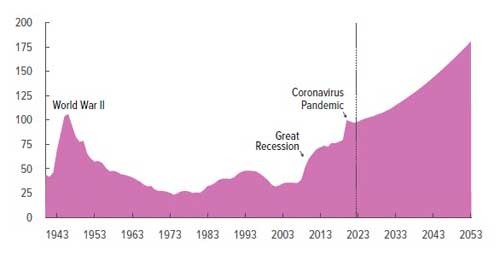

Today, US public debt hovers around $32.6 trillion; that’s two trillion more than a year ago. Since 2008, US debt as percentage of GDP has doubled and soared to over 120 percent. According to the non-partisan Congressional Budget Office, persistently large federal deficits will push federal debt over 181 percent of GDP by 2053.

Figure 3 US Federal debt held by the public

Source: CBO, June 2023

Avoiding lethal geopolitics

To defer the reckoning, the Biden administration needs to print money, ceaselessly. Such trajectories are damaging to major foreign holders of federal debt, many of which are large emerging economies, particularly China.

If, in a likely crisis, these economies must drastically reduce their purchases of US securities, sell a significant share of their dollar holdings, or do both, Washington needs to offset the gap. Otherwise, it will face significantly higher interest rates. Neither Western Europe nor Japan can alleviate the pain because they are struggling with secular stagnation, as is the US.

To avoid such lethal global scenarios, the BRICS seeks a diversified world economy and reserve currencies. That trajectory is more peaceful, stable and secure.

Dr. Dan Steinbock is an internationally recognized strategist of the multipolar world and the founder of Difference Group. He has served at India, China and America Institute (US), Shanghai Institutes for International Studies (China) and the EU Center (Singapore). For more, see https://www.differencegroup.net/

A version of the commentary was published by China Daily on August 23, 2023