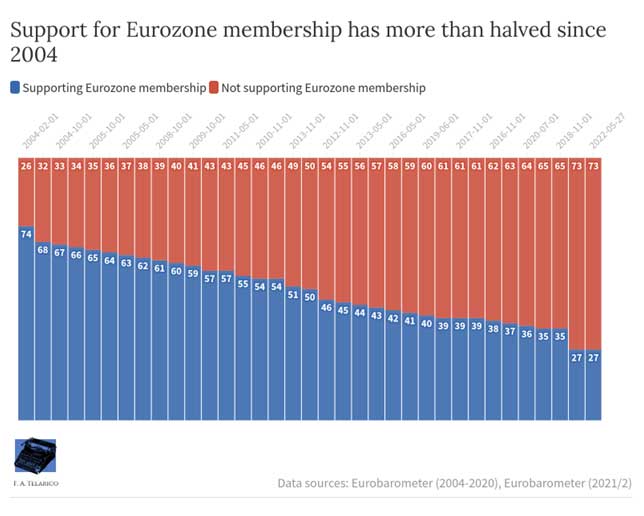

Bulgaria will adopt the euro in 2024 because ‘[t]he benefits […] outweigh the drawbacks’. At least, this is what Bulgaria’s finance minister, Asen Vasilev, argued to international media on June 3, 2022. Crucially, there is quite a lot of scepticism in the country regarding the real cost-benefit balance of the euro’s adoption. But the government has no intention of listening to the opposition by calling a vote on the parliament’s floor. Moreover, support for Eurozone membership practically more than halved from 74% in 2004 to 27% in 2022 (see chart below). Not to mention that the European Central Bank (ECB) itself found Bulgaria unfit for joining the Eurozone. Yet, there will not be a referendum asking voters whether they approve of this dramatic reform.

Indeed, there debate on the cons and pros of adopting the euro is mostly partisan and ideological. Hence, scrutiny of the government’s efforts to better align Bulgaria with the EU and the US remains seriously deficient.

Summary of the arguments in favour

Many of arguments in favour of adopting the euro are not actually country-specific. For instance, participating in the Eurozone can improve the quality of banking supervision for a country’s largest (‘systemically important’) banks. Additionally, economists have long argued that the use of a common currency is a key driver of investments and trade. Moreover, joining this exclusive club means gaining access to additional EU funds for pandemic-crisis relief.

But Bulgaria is also an intrinsically idiosyncratic country, especially when it comes to its fiscal and monetary policies. Namely, the local currency, called lev, is pegged to the euro at a fixed 1.98 exchange rate. Hence, some argue that Bulgaria is already in the Eurozone due to the currency board that guarantees the peg. Thus, becoming a Eurozone member would give Bulgaria’s central bank a say on the monetary decisions affecting the country’s economy.

Stay ahead of the geopolitical week.

MD Briefing delivers expert analysis across five global fronts — the Indo-Pacific, energy, geoeconomics, European security, and the Middle East — every Monday morning. Free.

Finally, more than 85% of Bulgarians has already used euro bills and/or coins. Thus, there is at least some familiarity with the common currency that may reduce unwanted side effects. And the government’s promised public messaging campaign to communicate the benefits of the euro may remedy the latter’s current unpopularity.

Arguments against

All too often, the arguments favouring the EU’s single currency are taken at face value. Instead, it is necessary to make them undergo a thorough dissection to distinguish assumptions from facts. For the sake of brevity, a few variables shall suffice to summarise the dynamics underlying Bulgaria’s peculiar cases.

Trade and investment

In Bulgaria’s cases, it is especially worth focusing on the potential impact of Eurozone membership on trade and investment. In particular, economists and politicians have consistently put the spotlight on how the euro facilitates foreign direct investments (FDIs). Coherently, Vasilev declared that ‘[j]oining the euro will […] boost investor confidence’ and help the Bulgarian economy grow faster.

However, there are many researches published by renowned institutions and universities disproving such claims. For instance, using data on 35 OECD countries covering the period 1997–2008, two Czech researchers found that ‘EU membership fosters FDI flows much more than the euro.’ Thus, the real booster to FDIs comes from a country’s membership in the EU, not the Eurozone. Similarly, two economists at the University of Amsterdam found ‘an estimated euro impact’ on trade in goods ‘of only 3%.’

Access to additional funds

True, joining the Eurozone would allow Bulgaria to access significant extra funding from EU institutions. However, there is a tendency to omit discussing the comparatively onerous costs of adopting the common currency. According to a well-known Bulgarian economists, Atanas Penkov, Bulgarian would pay an entrance fee between 1% and 3% of GDP.

Indicatively, the single largest expense would comprise upfront deposits for the European Stability Mechanism of up to €1.04bn. Essentially, Bulgaria would be paying 1–2% of its GDP to buy an insurance in case of insolvency. However, at less less than 30%, Bulgaria’s debt-to-GDP ratio is several times smaller than that of the average Eurozone country. Moreover, Bulgaria financed its public debt at relatively low interest rate (Figure 2). Thus, the risk of a public-debt crisis in Bulgaria in basically non-existent. Yet, the country would become ‘jointly liable for any problems’ in high-debt countries like Greece and Italy.

In addition, the State would lose all revenues from currency-exchange fees and incur logistic costs estimated at 0.3–7% of GDP.

Sovereignty and democracy

Lastly, there is issue of Bulgaria’s de-facto membership in the Eurozone and the benefits of having voting rights in the ECB.

There is one key fallacy in the arguments that adopting the euro would increase Bulgarian institutions’ influence on monetary policy. True, currently the Bulgarian central bank has no ability to influence monetary variables at its discretion. But Bulgarian political institutions do enjoy monetary sovereignty, they simply chose to delegate it for the time being. Indeed, one must remember that what ties the central bank’s hands is simply a law. Thus, future governments may change those rules or even repeal them altogether.

Meanwhile, there is no way back out of the Eurozone. Once Sofia delegates monetary sovereignty to Frankfurt there will be no government able to get it back. The government seems to be acutely aware of it, but this irreversible delegation of sovereignty does not generate any concern. Instead, Vasilev simply argued that crisis Greece’s crisis, which ‘nearly pulled the currency union apart […] shows that the currency’s flaws can be addressed’. However, he avoided to mention the immense costs that these ‘flaws’ can extol on the weakest members of society.

Conclusion: Beyond economics

Clearly, the approval of a plan to adopt the common currency is this government’s umpteenth top-down diktat. However, unlike previous such instances, this decision may weaken Bulgaria’s external independence. Namely, the definitive cession of monetary sovereignty will strengthen the ECB’s and other EU institutions’ role in economic policymaking. But, given the consistent push for more simple-majority decision-making, an apparently ‘technical’ decision may deal a fatal blow to Bulgaria’s very Statehood. Against this background, one ought to remember that the economics and politics of Eurozone membership is very complicated. And surely much more son than what this brief summary suggests. Nevertheless, it is undeniable that even bringing up such simplified arguments would benefit the debate in Bulgaria. Otherwise, the lack of sufficient public debate regarding the euro’s adoption may threaten the viability of Bulgarian democracy.