Getting to know Bulgaria’s “Fiscal Reserve”

Recently, Bulgarian commentators and policymakers have been whispering on the status of the “Fiscal Reserve”. This financial instrument is amongst the main indicators of Bulgaria’s economic stability. It is also a source the government draws from to finance extraordinary expenses without recurring to debt. Given the reserves’ importance, it is unsurprising that some wonder whether the government is wasting precious resources now and then.

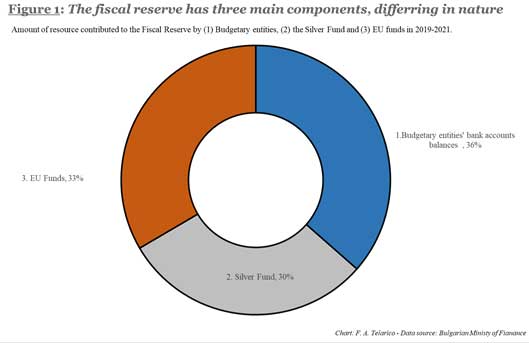

It is important to notice that Bulgaria’s fiscal reserve is actually an aggregate indicator which includes heterogenous sorts of components. Such a detail is actually essential because the government cannot earmark all of these resources freely for current expenditure. Thus, doubts relating to the fiscal reserve regard not just its level, but also its composition. To get a clearer picture, one may simply say that there are three main categories of assets in the fiscal reserve. First, budgetary institutions’ bank-account balances — which make up the lion share of the total. Second, the ‘Silver Fund’, a reservoir of assets meant to ensure the pension system’s sustainability, which is also quite significant. Finally, accounts receivable from European Union funds for certified expenses and advances, which have been rising steadily. On average, in 2019–2021 these three sources have provided the fiscal reserve with 99% of its value (Figure 1).

Lack of transparency contributes to make the issue even murkier. Publicly available information on the state and composition of Bulgaria’s fiscal reserve are rather incomplete. In fact, the Ministry of Finance only discloses the reserve’s total and a few other data on a monthly basis. Not even the ministry’s quarterly report on the fiscal reserve provides a better breakdown. Meanwhile, the issuance department of the Bulgarian National Bank (BNB) declares only total deposits weekly. Thus, worries on the status of the fiscal reserve appear justified overall.

Stay ahead of the geopolitical week.

MD Briefing delivers expert analysis across five global fronts — the Indo-Pacific, energy, geoeconomics, European security, and the Middle East — every Monday morning. Free.

More extraordinary expenses ahead

Like many other developed countries, Bulgaria has faced widening fiscal deficit due to the pandemic-induced crisis over the past year. The fiscal reserve’s erosion is the unavoidable result of reduced revenues’ and increases spending’s combined effect. Such a downward trend has led many to question public finances’ soundness and the government’s ability to manage the reserve. Moreover, as a caretaker cabinet replaced the previous executive after inconclusive elections scrutiny has intensified in May–June 2021.

In the next few months, the country has to face enormous expenses. This money is going to finance a €25 increase of all pensions as well as employment-support schemes. True, the government has foreseen a 4.9bln-leva deficit (ca. €2.5bln or $3bln) in the current fiscal year. However, is will probably not suffice to cover the cost of these and other measures, estimated at over €4.5bln. Actually, the very fiscal reserve from which the cabinet may want to draw may not be enough.

In fact, according to the latest available data, the Silver Fund sits at just a little over €1.7bln. Meanwhile, budgetary entities’ deposit with the BNB are somewhere in the realm of €3bln. Hence, despite the imminent collection of several taxes, the reserve would have to decrease drastically — something Bulgaria cannot afford. The only other option, is for the caretaker cabinet to finally manage to draft a revision of the budget. Yet, even in this case, there is no guarantee that after the elections in July the new parliament will pass it.

And the Fiscal Reserve keeps eroding

In the meantime, the size of the fiscal reserve keeps shrinking. Usually, its levels follow a sinusoidal trend, with periodical rises and falls. However, in the course of late 2020 and early 2021 revenues have systematically been insufficient to cover for past expenses. As such, each successive withdrawal has reduced the reserves’ total value incrementally. This divergence from established patterns is clearly visible in Figure 2, which disaggregates the fiscal reserve’s three main components.

As of May 2021, the fiscal reserve’s worth was €4.5 billion, as opposed to €5.2bln in May 2020 (Figure 2). In the short term, it had already gone down by €400mln, from €4.9bln in January of that year. Hence, the reserve shrunk twice as fast in January–May 2020 (-8.7%) than in the same period of 2021 (-4.2%). Simeon Djankov, deputy Prime Minister and Finance Minister in 2009–2013, argued already in mid-March that the government will have to withdrawal several further billion from the fiscal reserve. Similarly, Milen Velchev, finance minister in 2001–2005, argues that a new budget allow more borrowing is a priority.

Yet, the ousted prime minister’s party (GERB) is strenuously defending its financial track record and claiming their budget is sufficiently effective. Kiril Ananiev, former Finance Minister, noted that despite the deficit already high deficit, the fiscal reserve is still double its legal minimum. GERB’s leadership are argues that this is the worst state the reserve has ever been in. After all, in 2014 the fiscal reserve was worth only €2.6bln or 10% of GDP “without pandemic or extraordinary expenses”. Meanwhile, now reserves amount at 4.6% of GDP. Moreover, the reserve is on a deficit in the first quarter of 2021 for the first time.

Causes of a decline

As mentioned above, the official data on the fiscal reserve’s status tend to be rather fuzzy. But the Institute for Market Economy (IPI), one of the oldest Bulgarian think tanks, obtained disaggregated data for 2019-2021. These figures shed an interesting light on the interactions between fiscal policy and a stable fiscal reserve (Figure 3).

By February 28 2021, budgetary entities had about €2.7bln, €409mln of which destined to social security funds and EU-sponsored projects. In addition, the budget for 2021 earmarks €1.6bln for the Silver Fund; the least ‘liquid’ of the fiscal reserve’s three main components. As a result, there are just about €1.1bln available for discretionary spending. To get an idea, the current pension- and salary-support schemes have a combined cost of almost €110mln per month.

At their historical low-point, on August 31 2010, those accounts held €320mln, so the current situation is far from bleak. Yet, changes in the relative weight on the reserve’s total of its the three main components indicate several risks. As regards EU funds, they are rather stable in their absolute amount over the period January 2019–May 2021 (Figure 3). Generally, they fluctuate somewhere in the realm of €1.7–2.2 billion, averaging just under the €2bln mark. Nevertheless, their relative importance is usually quite unpredictable, and in steep rise since September 2020 (Figure 4). The same can be said of the Silver found, the value of which stands around €1bln. But excluding social-security funds, budgetary balances are at their lowest level for the entire period under review. Thus, their relative importance has decreased, making EU financing, pension funds and the Silver Fund significantly more important than before.

The peril ahead: Nationalising social-security funds

The danger could hardly be more evident. Without considerable free resources, the government will need to find new resources to finance any additional expense. Two are the main tools that would allow to replenish the reserve. First, generalised or target tax hikes may be sufficient on their own, or in combination with other tactics. However, they are out of question in this electoral period. Second, debt raised amongst domestic and international investors could be signed at relatively low interest rates. Yet, the current budget allows for no more than €2.3 billion of new-emission debt, which are unlikely to suffice.

Finally, the cabinet may repeat the script played out to save the reserve from its 2010 low. Back then, the government proposed the nationalisation of the National Health Insurance Fundj (NZOK). Since the parliament approved it, the State budget can draw freely on the billions in the NZOK’s balance. This time, nationalisers may eye the nationalisation Silver Fund – which also sustains social security – as the solution. Thus, they may amend the law destining assets in the Silver Fund to their current purpose to be able to finance urgent expenses. This would put high pressure on Bulgaria’s social security system and, potentially, expose present and future retirees to the risk of losing their hard-earned pensions.