When governments around the world started reacting to the pandemic, they induced a vast and unpredictable crisis. The ensuing recession struck in decidedly variegated ways both we looking at different countries and multiple social strata. Many economies fell in a downturn that has compromised access to income in certain States, although elsewhere these effects were risible. Such inequalities stand out in worldwide comparison, but they happen to be huge in structurally-alike, bordering States as well.

Recently, a varied pack of heavyweights and some smaller countries has rebounded strongly in relation to both GDP and employment. China and the US are at the forefront of this recovery for diverse whys and wherefores and in dissimilar manners. Like trucks on a difficult mountain road, the two are accelerating as they overcome the crisis helping the world economy.

Still, something is absent in this rubicund montage of rebounds and development: the European Union. Being the wealthiest market in human history, the EU may support other countries’ recovery tremendously. Yet, inner imbalances, organisational feebleness, and lack of resolve are restraining the Union. There have been serious consequences for some unconsolidated EU economies and on the many other States bound to the block. Following up a previous article, new data reveal how two very different country on the EU’s periphery fared in 2020.

Romania — The worst seems over

Over 20 million inhabitants and yearly exports worth about $80 billion make Romania a little giant in the Eastern Balkans. It joined the EU In 2007 in tandem with Bulgaria, and since analysts then to bundle the two countries together. However, this article’s approach is different as it compares Romania with the least populous country in the region: North Macedonia. The latter is not an EU member either, making them possibly the most dissimilar cases in the Eastern Balkans.

Stay ahead of the geopolitical week.

MD Briefing delivers expert analysis across five global fronts — the Indo-Pacific, energy, geoeconomics, European security, and the Middle East — every Monday morning. Free.

Romania’s economy suffered badly in the beginning of 2020, with its GDP collapsing 33% in the first quarter. These figures could be considered the worst since the onset of the post-socialist transition in the 1990s.The trend only got partially more positive in the following three months (April–June), when the economy started recovering somewhat. Yet, by the end of 2020 only 128,800 people had lost their job, or 1.49% on the previous year. The fact that the economy seems to be performing well has kept swaths of them in look for a new job. This explains rather discomforting unemployment statistics.

Gross Domestic Product

Romania’s economy only managed to get out of a steep slump in the summer quarter (July–September) of 2020. The figures reveal a strong V-shaped rebound, with GDP recovering almost 20 percentage points on its 2019 levels (Chart1). In the last three months of 2020, Romania’s GDP rose by a further 13%, reaching slightly above last years’ estimates. At the end of 2020, total production was 100.39% of its 2019 levels, whereas the Euro Area stopped at 96.86%.

Un/Employment

Curiously, unemployment data for most of 2020 diverge from Romanian economy’s overall impressive performance — and significantly so (Chart 2). Unemployment rose in the first three months of 2020, and started growing even faster in the ensuing nine months. In spite of a positive GDP dynamic, employment decreased by almost 130,000 units in 2020Q4due to the pandemic-induced crisis.

True, unemployment statistics do not say much about the structure of the Romanian labour market, a key factor in these processes. Unlike most of their Eurozone peers, Romanian enterprises deal with a greatly flexible manpower with fewer rights and protections. Thus, they can lay off and hire staff much faster than competitors and partners in the richest EU economies. Yet, one should not interpret unemployment’s as a consequence of new people entering the job market during 2020Q2–Q3. After all, in those six months the number of employed people fell by 2.4% compared to 2019Q3 or 207,500 units. Meanwhile, unemployment ‘only’ grew by 1.3 percentage points indicating that some laid-off workers became inactive. In a word, ordinary Romanians did not get a fair share of the recovery’s gains.

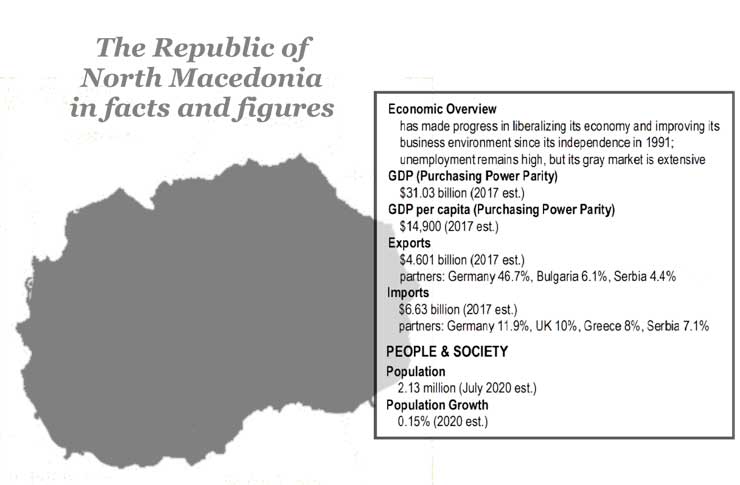

RNM — It couldn’t get much worse, so it got better

As anticipated, the Republic of North Macedonia (RNM) is very different from Romania in many respects. First, its population is a fraction of the latter’s, only about two million people according to questionable official data. Furthermore, the RNM is not a member of the EU despite the fact a markedly asymmetric dependence from the Union. In effect, its economy is mostly reliant on trade with and tourism from three EU member States: Bulgaria, Germany and Greece. The country averted a civil war in 2001 by appeasing its Albanian minority, but its economy has struggled ever since.

One could argue that the situation before the pandemic hit was so dire that worse performances were rather unlikely. When the economies of Bulgaria and Greece slowed down and tourism came to a halt, the RNM’s suffered as well. In the first quarter of 2020 the RNM’s GDP fell by 14%, and shrunk further in the following three months. New figures show that about 17,000 people lost their job in April–June 2020, which became 21,000 in December. This means a 2.66% decrease in employment for a country where unemployment was 17.3% in 2019.

Gross domestic product

The RNM’s economy took the biggest hit in the second quarter of 2020, after having already suffered somewhat in January-March. In 2020Q2, North Macedonian GDP was about 23% lower than in 2019 (Chart 3), against the Eurozone’s 17%.Yet, the slid is nothing like the recession the RNM experienced during the Yugoslav Wars and the 2001 civil war. With the summer, both Bulgaria and Greece as well as the entire EU reopened their borders and started growing again. There were positive ripple effects on the RNM’s economy in the third quarter, with GDP growing by 448 million euros. The 20% increase of the summer became the base for further growth in the October-December 2020. By the end of the fourth quarter, the RNM’s GDP increased by another 10%— converging on its 2019 levels.

Un/employment

Unlike in Romania’s case, inconstant performances did not affect unemployment statistics visibly in the RNM (Chart 4). Actually, and counter intuitively, in comparison to 2019 unemployment decreased by 0.6% to 16.7% in the first two quarters of 2020. In total, during the first half of 2020, the RNM’s economy lost4,200 jobs or 0.5% in comparison to 2019 levels. The National Statistical Agency recorded similarly inconclusive fluctuations all year round, suggesting a deep disconnect between GDP and unemployment. All in all, one could justify these findings with the ignominious state in which the RNM’s labour market is. The population is not very active, yet unemployment has never fallen below 15%in the past 20 years. Therefore, ordinary people fail to reap sensible benefits even if the economy overall is growing.

Conclusion: Pandemic management matters

There are two lessons that one can draw from these figures and by comparing the cases of Romania and the RNM. One, regards the pandemic and the ways its management interact with key economic indicators. While the other speaks volume on the differences between these two countries on the EU’s periphery.

Arguably, the data may comfort the thesis that not only lockdown fuel recessions, but less lockdowns spur economic growth. In fact, Romania performing better than most EU and Eurozone economies in terms of GPD growth suggests that less lockdowns favour growth. After all, authorities in Bucharest have been and remain remarkably consistent in their refusal to shut down the economy. Conversely, the rather trendless fluctuation in the RNM’s data and performance results at least partly from the government’s inconsistency. Actually, Skopje went from minimal anti-contagion restrictions to declaring a full-scale, countrywide lockdown virtually overnight— a behaviour that fuels uncertainty.

Additionally, these figures dispel some of the cloud surrounding the EU’s and its peripheries’ path out of the crisis. On the one hand, the EU is trying to dig its escape route by investing billions of euros over the coming years for countrywide Recovery plans. True, Romania’s share of grants is not as bis as Bulgaria’s, Greece’s or Italy’s, but the government is thinking big. On the other hand, the RNM is amongst the “poorest countries in Europe” never to be part of the USSR. Unemployment figures could cause vertigos even before the pandemic hit and the population is shrinking at impressive rhythms. Not being a member of the EU, Skopje will get only a fraction of the money Brussels has earmarked. Paradoxically, dependence on the EU was the transmission belt of the crisis, but lack of integration will hinder the recovery.