This article explores systemic and market barriers preventing the wider use of BRICS national currencies in trade, including currency swaps mechanisms and reasons for BRICS exporters’ preference not to use national currencies. Design flaws are outlined in the New Development Banks’ Contingency Reserve Arrangement (CRA) in the context of de-dollarizing BRICS trade, namely its IMF linkage requirements and limited scope, symptomatic of a lack of trust between BRICS member states. The current levels of de-dollarization in Russia’s intra-BRICS settlements (as a representative sample) are used to find gaps between Russia’s stated de-dollarization goals and current initiatives, and market barriers are identified to explain this gap. Finally, the components of market mechanisms needed to de-risk Intra-BRICS trade and overcome the identified barriers are outlined.

Background to Challenge

The 2017 BRICS New Development Bank’s strategy report The Role Of BRICS In The World Economy & International Development detailed a long-term vision of the direction BRICS countries’ economic cooperation was headed in. The strategy report made the case that reforms in the existing western institutions would not be in BRICS countries’ favour in the near future, and hence emphasized the importance of a new Multilateral Clearing Union (MCU) which would serve as an intra-BRICS currency swap pool and tackle balance of payment shortcomings, trade finance, financial crisis aversion, and an overall restoration of sovereignty by de-dollarizing BRICS trade (NDB, 2017). This intention was also echoed in the 2017 BRICS Xiamen Summit declaration, which stated:

“We agree to …enhance currency cooperation, consistent with each central bank’s legal mandate, including through currency swap, local currency settlement, and local currency direct investment….We commend the progress in concluding the Memoranda of Understanding among national development banks of BRICS countries on interbank local currency credit line and on interbank cooperation in relation to credit rating.”

Stay ahead of the geopolitical week.

MD Briefing delivers expert analysis across five global fronts — the Indo-Pacific, energy, geoeconomics, European security, and the Middle East — every Monday morning. Free.

In parallel to the Xiamen summit, the R5+ (Real, Ruble, Rupee, Renminbi, Rand, in addition to the currencies of BRICS+ countries) currency initiative was launched, which sought to stimulate the use of national currencies for “investments, long-term projects, creation of common payment card systems and common settlement/payment systems, cooperation in promoting BRICS+ currencies towards reserve currency status.”

The New Development Bank’s proposed Multilateral Clearing Union was manifested in the form of a $100 billion Contingency Reserve Arrangement (CRA) that BRICS countries devised as a pool to swap currencies in times of need, increasing national currency settlement. The CRA included two currency swap instruments to support short-term balance of payment (BoP) pressures between a country’s current and capital accounts: 1) a liquidity instrument to provide support in response to current BoP gaps, and 2) a precautionary instrument to buffer against future BoP gaps. A country’s access to the shared capital funds was limited by conditionality, as only 30% of accessible funds (“de-linked portion”) were available on demand, whereas the majority, 70% of accessible funds require on-track arrangements with the IMF, as the CRA’s rationale document explains:

“Where financing in excess of this 30% limit is required, an ‘IMF-linked portion’ will be made available. This will allow the country access to the remaining 70%, provided that a conditionality-based agreement with the IMF is concluded” (Biziwick, M., Cattaneo, N. and Fryer, D., 2015 (p. 316)).

CRA Defects

Of importance, it is worth noting that rather than having a mechanism for direct currency swaps, a swap transaction was defined as “the Requesting Party’s central bank purchases US dollars (USD) from the Providing Party’s central bank in exchange for the Requesting Party Currency, and repurchases on a later date the Requesting Party Currency in exchange for USD” (Biziwick et al., 2015 (p. 316)).

As a result, the CRA’s IMF linked component and USD reserve currency status raise questions about whether there is a potential mismatch between the stated goals of the MCU and the CRA’s implementation mechanism. In the RISS Joint Research Paper Use of national currencies in international settlements: Experience of the BRICS countries, Karataev et al state:

“Though the BRICS countries have established a Contingent Reserve Arrangement… the currency swap under this arrangement is one between US dollar and local currencies of BRICS, not one among the BRICS currencies. Currently, there are few local currency swap agreements in force (between Russia and China, China and South Africa)” (Karataev et al., 2017 (p.110).

The key barriers hindering the CRA’s success towards its stated goals, including the CRA’s promissory model, limited size (mirroring the limited paid-in capital allocated to BRICS’ New Development Bank), and IMF linking, stem from the CRA modelling itself after the ASEAN+3 Chiang Mai currency swap initiative, which had a limited scope, operated on a promissory model rather than an actual capital pool, and carried a significant IMF-linked portion due to the lack of financial surveillance capacity and moral hazard borrowing risk (Biziwick et al., 2015 (p. 318)). On a macro level, “the CMI/CMIM arrangement has been criticized as utterly ineffective (it did not play any role in the 2008 crisis, for example), and the concern is that, by adopting its form, the CRA is condemning itself to a similar fate. Size and IMF linking (along with the lack of a rapid response facility) seem to have been major problems with the CMI/CMIM arrangement…the IMF linking seems hard to reconcile with the intention to provide a counterweight to the IMF ” (Biziwick et al., 2015 (p. 318)). Thus, as was the case with the Chiang Mai currency swap initiative, the BRICS NDB’s CRA’s promissory model, limited size (mirroring the limited paid-in capital allocated to BRICS’ New Development Bank), and IMF linking all stem from a fundamental lack of trust between BRICS member countries on their self-reliance for monitoring and governance of each others’ and common funds.

Despite their stated desire to break away from IMF’s conditionalities and dollar-denominated trade, at least in the CRA, a greater trust has been placed in the IMF for monitoring conditions for credit swaps. BRICS countries have thus inadvertently followed precedents set by hegemons.

This status quo is not inevitable, and can easily be overcome by coordinated CRA reform to introduce an internal trust-ensuring credit mechanism amidst financial instruments in national currencies to build the foundation for true independence from IMF and dollar-denominated transactions.

Market barriers to BRICS Trade De-Dollarization:

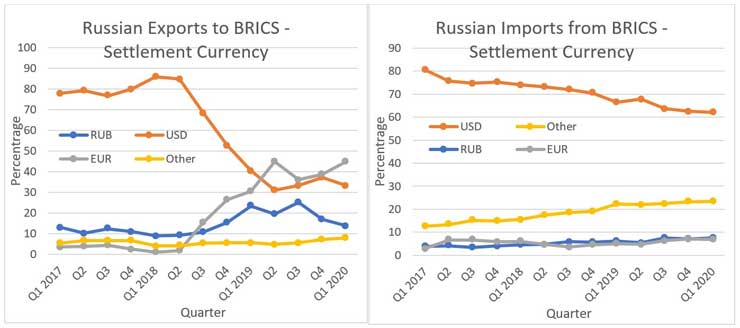

In addition to the CRA design flaws, BRICS Trade De-Dollarization is also held back by market barriers. As a representative sample to measure progress in de-dollarization, the currency composition of Russia’s publicly available intra-BRICS trade settlement since the launching of prominent de-dollarization initiatives in 2017 can be examined, as shown in figure 1 below. The percentage of Russian exports to BRICS countries settled in dollars has fallen from its peak of above 80% in Q1 2018 to 33.2% as of first quarter of 2020 (CBR, 2020). While Russian exports to BRICS have de-dollarized recently, it is apparent that rather than BRICS currencies, the Euro has replaced the dollar as the dominant export settlement currency (Russia is receiving only 13% of its exports in Rubles as of Q1 2020).

Figure 1: Settlement Currency Percentage for Russian Exports to BRICS (CBR, 2020)

This is due to Russian energy exporters preferring to denominate contracts in Euros rather than Rubles recently, for the same reason they previously preferred to denominate contracts in Dollars: greater volume of Rubles received in case of depreciation. By contrast, Russian imports from BRICS countries are still largely settled in Dollars as of Q1 2020, though there is a gradual de-dollarization trend present. The “other” currency slowly rising in imports settlements most likely being largely comprised of the Renminbi Yuan, as China and Russia have been accelerating ruble and yuan use in trade since 2019. Despite this, as demonstrated in Figure 1, it is worthy to note that Russia’s inter-BRICS trade is by far settled mostly in Dollars and Euros rather than Rubles or any other BRICS currency, indicating a gap of between Russian traders’ settlement currency choice and BRICS de-dollarization priorities.

To explain this phenomenon in greater detail, Karataev et al. outlined two key fundamental market barriers preventing the use of national currencies for BRICS trade finance specifically which need to be overcome as a supplement intra-BRICS currency swaps:

1. Currency Volatility:

Exchange rate fluctuations create uncertainty in optimizing settlement pricing and profitability at time of contract fulfilment from both exporters’ and importers’ perspective- “Exporters will seek to denominate their contracts in foreign exchange when their national currency is devaluing. It will allow them to receive additional profits in the national currency…(whereas) importers shall be encouraged to invoice a contract price in their national currency in order to reduce costs and prevent a decline in demand as a result of rising prices.” (Karataev et al., 2017 (p.20)).

2. Global Commodity Benchmarks:

“Exporters of similar goods [i.e. commodities]… will seek to establish the contract price in the same currency as their competitors. That allows them to neutralize more successfully the adverse exchange rate fluctuations resulting in considerable price changes and therefore prevent the risk of reducing demand. As a result, the market price of such goods is denominated mostly in the US dollar….the global commodities exchange trade in these goods plays a significant role…if the global commodities market’s impact on the pricing model will decrease, the use of the USD as invoicing currency will decline too.” (Karataev et al., 2017 (p.19)).

Thus, the dominant factors preventing BRICS currency usage in trade were exchange rate fluctuations causing exporters to optimize profit margins by using foreign exchange (typically denominated in dollars), and industry benchmarks for export goods pricing, especially the influence of global commodities exchanges denominated in dollars. Amongst BRICS countries, this holds true for the largest Russian energy exporters, who often prefer to be paid in dollars or euros in order to maintain standardized price points and obtain additional rubles in case of depreciation.

However, empirical research demonstrated by Nakajima et al. with the vine copula method and value-at-risk model has found that using BRICS currencies in energy trade resulted in more stable prices and avoided translation risks compared to using dollars due to counter-balancing movements with oil prices (Nakajima et al, 2020). Thus, though dollar-denominated oil contracts may provide short-term gains for exporters, the overall commodity trade between BRICS countries would benefit from the use of national currencies. In addition, though the Euro is replacing the Dollar as Russia’s preferred export settlement currency within BRICS, the Euro poses lesser but similar risks to being weaponized by sanctions, given that it is still a third party non-BRICS currency and European Union sanctions against Russia could be expanded in the near future in light of political events unfolding in 2020 (i.e. EU-Russia differences over Belarus protests, Navalny incident, etc.).

Current Steps:

To overcome the remaining barriers to using national currencies, current steps being taken in BRICS include developing an in-house settlement system for trade finance based on Russia’s SPFS alternative to SWIFT, linking domestic payment systems to create the New International Payment System (NIPS), and researching feasibility requirements towards a common BRICS cryptocurrency. In addition, while progress has been made in diversifying the NDB’s loan denominations to include more local currencies, with a goal of 50% project financing in the near future according to NDB’s president, the more widespread internationalization of BRICS currencies would require mature bond markets to be created in all BRICS countries to compete with western bond markets. This was initiated by the creation of BRICS Local Currency Bond Fund during the 2017 BRICS Xiamen Summit declaration:

“We agree to promote the development of BRICS Local Currency Bond Markets and jointly establish a BRICS Local Currency Bond Fund, as a means of contributing to the capital sustainability of financing in BRICS countries, boosting the development of BRICS domestic and regional bond markets, including by increasing foreign private sector participation, and enhancing financial resilience of BRICS countries.“

Though these steps are cumulatively designed to increase autonomy over intra-BRICS fund flows, they do not, however, address the fundamental gap in de-risking the barriers to using national currencies in BRICS settlements which are holding back their more widespread use. Central Bank of Russia Governor Dr Elvira Nabiullina echoed this sentiment in 2019 when she claimed that while gold-pegged cryptocurrencies are being researched, it was more important to develop international settlements using national currencies. Thus, while BRICS payment and settlement systems are being integrated, BRICS local bonds are being developed, direct currency swap lines are being expanded, and an intra-BRICS cryptocurrency architecture conceptualized and brought to market, a crucial intermediate supplementary step in de-dollarizing inter-BRICS trade finance is establishing de-risked and mutually trustable intra-BRICS trade contracts to expand national currency settlement, overcoming the market barriers mentioned previously.

Gap Identification: Steps Needed for De-Risking Trade

Karataev et al. proposed a multi-tiered circular system whereby national and intra-BRICS financial institutions complement and coordinate with BRICS trade settlement transactions to create a robust system for using local currencies. The components steps were outlined as follows: 1) direct currency trading expansion and lowering transactions costs 2) creation and use of hedging instruments in BRICS currency pairs which would reduce risk management costs 3) widening of Swap Agreements and limiting liquidity risk, 4) local currency bond market development in conjunction with trade and development goals 5) trade surplus re-investment into local bond markets 6) diversification of bond markets and BRICS policy coordination for using these instruments to achieve currency internationalization goals (Karataev et al., 2017 (p. 111)).

Out of these measures, the CRA was designed to meet the needs of step 3, whereas progress has been started on steps 4-6 by the New Development Bank based on initiatives launched during the Xiamen summit. However, concrete initiatives are needed to fulfil steps 1 and 2. Karataev et al. specified three key exchange mechanisms in particular which need to be established to lower transaction costs and de-risk the use of national currencies in intra-BRICS trade contracts to overcome the aforementioned barriers for steps the first two steps mentioned above:

- BRICS Interbank foreign exchange market, whereby “companies should be able to purchase/sell a currency quickly and without additional costs to make settlements in such currency. This presumes the existence of a highly developed and liquid interbank and forex markets with large numbers of participants and convertible financial instruments” (Karataev et al., 2017 (p.18)).

- Currency Hedging instruments — “It will be necessary to encourage trading directly in BRICS currencies that will significantly contribute to lowering costs. This step [BRICS Trading pairs] has to be augmented with the creation and use of hedging instruments in BRICS currency pairs which might allow to reduce risk management costs. During the first stage leading public banks of BRICS countries may function as market makers on currency pairs to provide necessary liquidity.” (Karataev et al., 2017 (p.110)).

- BRICS Commodify Exchange — “Launching of a Commodity Exchange or some type of an e-trading platform for trade in goods and derivatives of various kinds can be one more instrument contributing to enhancing LCY [local currency] use in settlements in the BRICS countries…raw material trade could be mediated by setting market prices denominated in local currencies. With appreciable quantity of foreign investors trading on the exchange, this will lead to the internationalization of contracts denominated in local currencies” (Karataev et al., 2017 (p.112)).

In addition to the above three suggested exchanges, intra-BRICS trade de-dollarization requires the IMF-linked portion of the CRA to be removed to enable direct currency swaps to take place, granted the existence of bilateral swap agreements between all BRICS countries. A necessary replacement for the IMF on-track arrangement must be established between BRICS countries: a counter-party de-risking mechanism which serves as an independent source of trust to validate the fulfilment criterion of trade-necessitated direct currency swaps, thus eliminating the need for IMF on-track arrangements and consequent USD conversion.

Currently, all BRICS countries are largely reliant on western facilities for the above four types of exchanges. SWIFT largely dominates international interbank transfer settlement, with the Russian and Chinese SWIFT alternatives operating mostly domestically, though there are plans for integration of BRICS settlement systems as mentioned previously. BRICS countries have yet to develop a comprehensive intra-BRICS hedging mechanism for mitigating currency volatility risk directly independent of dollar and euro-denominated western capital markets.

Conclusions and Recommendations:

BRICS countries have maintained a longstanding goal of de-IMFing and de-dollarizing their trade settlements and reserves in order to increase their sovereignty over transactions and avoid currency crisis, and proposed the creation of a Multilateral Clearing Union towards that goal. However, design flaws in the Multilateral Clearing Union, a lack of an independent credit monitoring mechanism, and lack of currently de-risking mechanisms in intra-BRICS trade finance prevented the wider use of national currencies.

To overcome the reluctance of BRICS traders to take trade finance loans and settle in BRICS national currencies, there is a need to introduce forward hedging options with minimal cost of carry so traders can avail direct hedging options simultaneously with trade contracts to de-risk their trade contract in national currencies. As Karatev et al. concluded, in the long term goal, boosting demand for direct BRICS currency settlement would itself partially smooth out some of the volatility experienced by cyclical western capital flight, thus lowering the risk premium and cost of carry for forward contracts, making BRICS currencies the natural preferred choice in trade finance (Karataev et al., 2017 (p.110).

After a currency options market, a BRICS commodity exchange specifically needs to be created in which commodity prices are denoted in national currencies, and are accompanied by derivatives and other risk hedging options that minimize the combined effects of currency and commodity price fluctuations, essentially serving as a favoured market for BRICS commodity importers and exports to set contracts in national currencies and have instruments to de-risk any expected volatility. The most significant example of a local currency commodity exchange within BRICS was the Petro-Yuan futures market launched in China in 2016, which served as a viable alternative to the dominant dollar-denominated WTI and Brent oil exchanges. Though Russia has set up a similar exchange in the form of the Ural Oil Futures market, work remains to be done to achieve maturity and usage to the level of established commodities exchanges.

Combined with direct currency swap lines and an intra-BRICS free trade zone, the implementation of the above mechanisms would lower the transaction cost of BRICS national currency trade settlement, by lowering the risk premium for importers and exporters to set contracts in national currencies amidst exchange rate uncertainty. Thus, these exchanges would fulfil the BRICS goals of “focus[ing] joint efforts on providing companies engaged in foreign trade from BRICS countries with the same, or lower transaction (compliance) costs, guarantees of settlement and risk management that they currently have in utilizing the dollar, euro or yen” (Karataev et al., 2017 (p.110-111)).

In 2018, export-oriented development banks from all BRICS countries signed a MoU to enhance understanding of distributed ledger or blockchain technology for solving challenges in trade finance, with the aim of identifying areas to improve operational efficiencies and tackle common financial challenges. In 2019, the BRICS Business Council formed a working group exploring how a special trade-facilitating BRICS crypto-currency could be created to ensure the smooth flow of paperless document flow for trade obligations.

In fact, creating a specialized crypto-currency for document flow is not necessary to meet the BRICS goal of de-risking national currency trade settlement. The simplest yet most advanced and low-cost blockchain feature to enable the above four exchanges to take place directly between BRICS traders and banks (and allow a seamless disintermediation of transactions between separate parties without the need for outside third parties such as IMF) are Smart Contracts, an original feature of Ethereum networks but later adapted by other blockchain networks. Smart Contracts allow for multiple parties to program and pre-set conditional criterion for contracts based on fulfilment of services or market conditions, and automate the verification of fulfilment criterion via decentralized external verification engines known as Oracles, which are blockchain middleware that create a secure connection between Smart Contracts and various off-chain resources required for fulfilment. Funds needed to execute the contract can be temporarily pre-stored in a linked virtual escrow-like account associated with the contract to guarantee fund availability at the time of execution. Once the contract execution date arrives and conditional fulfilment checks have been completed, Smart Contracts self-execute and disburse associated payments to the contracting parties, automating execution and settlement and eliminating contract disputes and counter-party non-fulfilment risks.

Due to their automated fulfilment capabilities and dis-intermediation of third party legal and settlement entities, Smart Contracts are starting to be gain traction in western consortiums for trade finance, currency trading, and commodity trading in the mainstream dollarized economy. Trade Finance systems based on Smart Contract are currently enabling on average a 35% reduction in costs and the elimination of the 1–2 weeks of processing time for settlements, in addition to removing room for manual errors.

The author has proposed a solution implementing the above exchanges using Smart Contracts to De-Risk and De-Dollarize Intra-BRICS Trade—further details on this solution beyond those mentioned in this article can be seen in the December 2020 issue of the BRICS Journal of Economics.

Printed Sources Cited:

- Biziwick, M., Cattaneo, N. and Fryer, D. (2015) “The rationale for and potential role of the BRICS Contingent Reserve Arrangement.” South African Journal of International Affairs. 22:3, 307-324.

- Central Bank of Russia Trade Finance Settlement Data. “Credit Statistics” http://www.cbr.ru/vfs/statistics/credit_statistics/cur_str.xlsx translated into English, plotted in Excel.

- Nakajima, Tadahiro, Yijin, He and Hamori, Shigeyuki. (2020). Can BRICS’ currency be a hedge or a safe haven for energy portfolio? An evidence from vine copula approach. The Singapore Economic Review. 65(4) 805-836. https://doi.org/10.1142/S0217590820500174.

- NDB – New Development Bank. (2017) “The Role Of BRICS In The World Economy & International Development” BRICS New Development Bank Strategy Report. https://reddytoread.files.wordpress.com/2017/09/brics-2017.pdf.

From our partner RIAC