With the COVID-19 pandemic continuing to threaten jobs, businesses and the health and well-being of millions amid exceptional uncertainty, building confidence will be crucial to ensure that economies recover and adapt, says the OECD’s Interim Economic Outlook.

After an unprecedented collapse in the first half of the year, economic output recovered swiftly following the easing of containment measures and the initial re-opening of businesses, but the pace of recovery has lost some momentum more recently. New restrictions being imposed in some countries to tackle the resurgence of the virus are likely to have slowed growth, the report says.

Uncertainty remains high and the strength of the recovery varies markedly between countries and between business sectors. Prospects for an inclusive, resilient and sustainable economic growth will depend on a range of factors including the likelihood of new outbreaks of the virus, how well individuals observe health measures and restrictions, consumer and business confidence, and the extent to which government support to maintain jobs and help businesses succeeds in boosting demand.

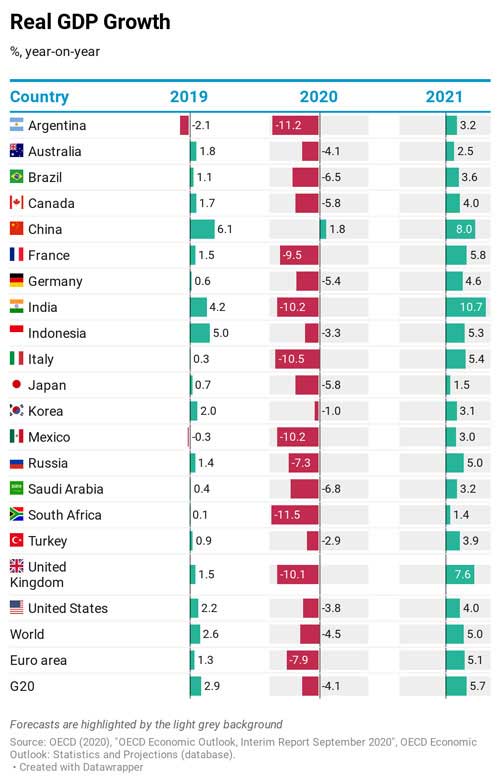

The Interim Economic Outlook projects global GDP to fall by 4½ per cent this year, before growing by 5% in 2021. The forecasts are less negative than those in OECD’s June Economic Outlook, due primarily to better than expected outcomes for China and the United States in the first half of this year and a response by governments on a massive scale. However, output in many countries at the end of 2021 will still be below the levels at the end of 2019, and well below what was projected prior to the pandemic.

Stay ahead of the geopolitical week.

MD Briefing delivers expert analysis across five global fronts — the Indo-Pacific, energy, geoeconomics, European security, and the Middle East — every Monday morning. Free.

If the threat from COVID-19 fades more quickly than expected, improved business and consumer confidence could boost global activity sharply in 2021. But a stronger resurgence of the virus, or more stringent lockdowns could cut 2-3 percentage points from global growth in 2021, with even higher unemployment and a prolonged period of weak investment.

Presenting the Interim Economic Outlook, covering G20 economies, OECD Chief Economist Laurence Boone said: “The world is facing an acute health crisis and the most dramatic economic slowdown since the Second World War. The end is not yet in sight but there is still much policymakers can do to help build confidence.”

She added: “It is important that governments avoid the mistake of tightening fiscal policy too quickly, as happened after the last financial crisis. Without continued government support, bankruptcies and unemployment could rise faster than warranted and take a toll on people’s livelihoods for years to come. Policymakers have the opportunity of a lifetime to implement truly sustainable recovery plans that reboot the economy and generate investment in the digital upgrades much needed by small and medium-sized companies, as well as in green infrastructure, transport and housing to build back a better and greener economy.”

The report warns that many businesses in the service sectors most affected by shutdowns, such as transport, entertainment and leisure, could become insolvent if demand does not recover, triggering large-scale job losses. Rising unemployment is also likely to worsen the risk of poverty and deprivation for millions of informal workers, particularly in emerging-market economies.

The rapid reaction of policymakers in many countries to buffer the initial blow to incomes and jobs prevented an even larger drop in output. The Interim Outlook says it is essential for governments not to repeat mistakes of past recessions but to continue to provide fiscal, financial and other policy support at the current stage of the recovery and for 2021. Such measures should be flexible enough to adapt to changing conditions and become more targeted.

Continued state support needs to be increasingly conditioned on broader environmental, economic and social objectives. Better targeting of support to where it is needed most will improve prospects, particularly for the unemployed and the low skilled – groups who too often miss out on training – and for youths. The report acknowledges that a balance needs to be struck between providing immediate support to strengthen the recovery while encouraging workers and businesses in hard-hit sectors to move into more promising activities.

Support also needs to be focussed on viable businesses, moving away from debt into equity, to help them to invest in digitalisation, and in the products and services our society will need in the decades ahead. Far stronger commitment needs to be devoted to address climate change in recovery plans, in particular conditioning support on greater investment in green energy, infrastructure, transport and housing.

At the same time, and with the virus continuing to spread, investing in health professionals and systems must remain a priority. The OECD says global co-operation and co-ordination are essential, as greater funding and multilateral efforts will be needed to ensure that affordable vaccines and treatments will be deployed rapidly in all countries when available.

The release of the Interim Economic Outlook follows an OECD Ministerial Roundtable at which Secretary-General Angel Gurría called for countries to go further in greening the stimulus packages they have announced to tackle the impact of the COVID-19 crisis in order to drive sustainable, inclusive, resilient economic growth and improve well-being.

“Climate change and biodiversity loss are the next crises around the corner and we are running out of time to tackle them,” he said. “Green recovery measures are a win-win option as they can improve environmental outcomes while boosting economic activity and enhancing well-being for all.”