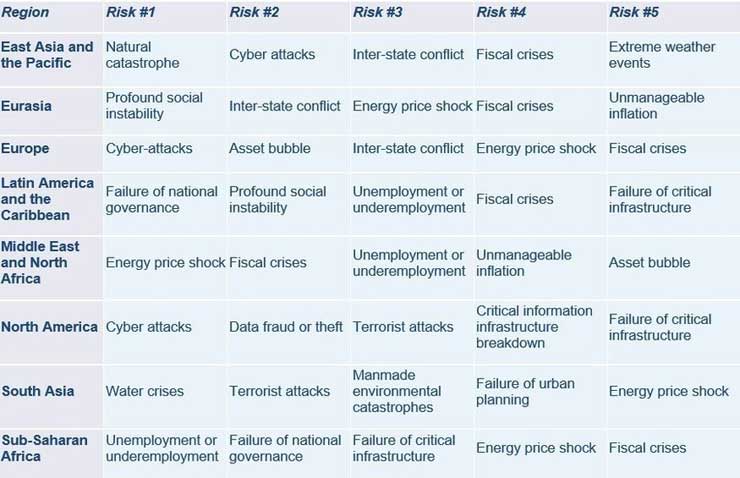

Economic issues dominate concerns for business executives around the world, according to the World Economic Forum’s Regional Risks for Doing Business 2019 report. In a survey of nearly 13,000 business leaders in over 130 countries, respondents ranked “fiscal crises” as the leading risk to doing business at a global scale.

Globally, three of the top five risks are economic-related with “unemployment or underemployment” coming in third and “energy price shock” ranking fourth. These risks have strong links to social disruption and contribute to “failure of national governance” ranking fifth and “profound social instability” ranking sixth. “Cyberattacks” are the second biggest challenge for executives, and the most important one for European and North American businesses for the second year in a row, highlighting the increased sophistication and proliferation of this type of attack.

Environmental-related risks are the top concerns in South Asia and in East Asia and the Pacific, with both regions having suffered devastating natural disasters and extreme weather events. Social challenges rank high in Eurasia, affected by economic slowdown, and Latin America and in the Caribbean, where governments are still aiming to deliver critical social services.

In the Middle East and North Africa “energy price shock” leads due to ongoing price and production volatility, and in sub-Saharan Africa, where youth unemployment is above 13%, executives are worried by their economies’ inability to create jobs. While global cooperation is still the most effective tool to address these varying risks, the report’s mapping highlights the areas in which regions can act.

Stay ahead of the geopolitical week.

MD Briefing delivers expert analysis across five global fronts — the Indo-Pacific, energy, geoeconomics, European security, and the Middle East — every Monday morning. Free.

“At a time when global economic growth appears fragile, business leaders are deeply concerned by their governments’ fiscal resilience. Meanwhile, cyberthreats remain a major risk due to their rapid evolution and increasingly disruptive potential,” said Emilio Granados-Franco, Head of Global Risks and Geopolitical Agenda at the World Economic Forum. “But in examining risk at the regional level, we also see various, interconnected drivers shaping diverse risks landscapes. Only by addressing economic risks and societal, technological, and environmental risks in an integrated manner, can stakeholders truly build resiliency.”

John Drzik, President of Global Risk and Digital at Marsh, said: “Cybersecurity remains the most concerning risk to business leaders in advanced economies, and growing technology dependence for many businesses will only amplify this. Combined with fractious geopolitical developments, and growing economic concerns, executives face a very challenging portfolio of potential threats. Business leaders should reevaluate their underlying view of the global risk environment and make greater efforts to strengthen their corporate agility and resilience.”

“There is a real existential threat to businesses worldwide,” said Eugenie Molyneux, Chief Risk Officer Commercial Insurance, Zurich Insurance Group. “Executives are concerned that governments have too much debt to be able to afford measures that could help avoid a recession, and see cyberattacks as the number one risk in 16 economies representing over 40% of the world’s GDP. At the same time, businesses are not even factoring in the impact of climate change over the next decade. These three risks need urgent action.”

The Regional Risks for Doing Business 2019 report is published in partnership with Marsh & McLennan Companies and Zurich Insurance Group and is part of the Forum’s Global Risks Initiative – a workstream that analyses critical global risks and communicates these risks to stakeholders and the wider public through digital and media assets.

Methodology

The findings of the Regional Risks for Doing Business 2019 report are based on 12,897 responses from executives in 133 economies. Respondents were asked to select “the five global risks that you believe to be of most concern for doing business in your country within the next 10 years”. This question is included in the annual Executive Opinion Survey, which is a part of the World Economic Forum’s Global Competitiveness Report. The latest edition of the survey was carried out from January to April 2019. Business leaders were asked to choose up to five risks from a list of 30, including terrorist attacks, extreme weather events and state collapse or crisis.