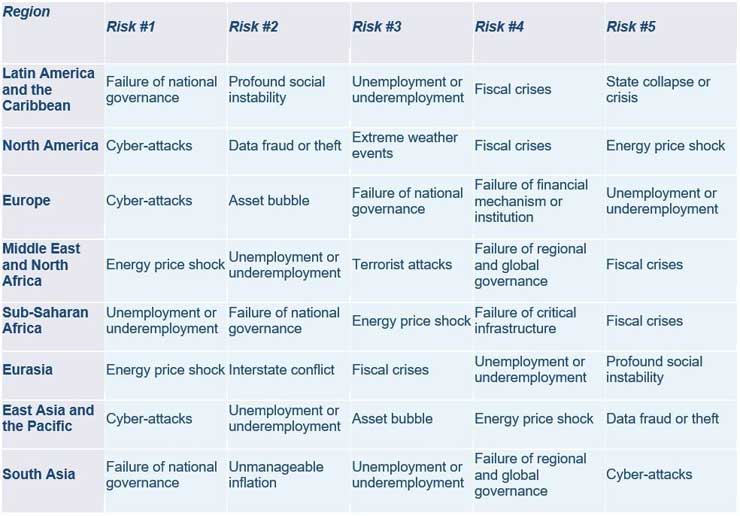

There are significant differences in risk perceptions across the eight regions covered in the World Economic Forum’s Regional Risks for Doing Business report. Over 12,000 executives highlighted concerns ranging from economic to political, societal and technological. Unemployment, failure of national governance and energy price shocks were among the top worries of executives across various regions.

Cyber-attacks are the number one risk in Europe, East Asia and the Pacific and North America. This points to growing concerns about technological risks – cyber-attacks were the top risk in two regions, according to the 2017 survey (East Asia and the Pacific and North America), and only one region in 2016 (North America).

Failure of national governance ranked number one in Latin America and South Asia, highlighting the costs of political strains that have been evident in much of the world in recent years. In the energy-rich regions of Eurasia and Middle East and North Africa, energy price shocks were ranked as the top risk to doing business. Unemployment was perceived as the top risk for doing business in sub-Saharan Africa, representing mostly the absence of demand in the region.

“Given the current geopolitical uncertainty globally, cooperation within and among regions is of critical importance. Understanding the evolving risks in different regions is therefore top of mind for business leaders,” said Mirek Dusek, Deputy Head of Geopolitical and Regional Agendas and Member of the Executive Committee at the World Economic Forum.

Stay ahead of the geopolitical week.

MD Briefing delivers expert analysis across five global fronts — the Indo-Pacific, energy, geoeconomics, European security, and the Middle East — every Monday morning. Free.

“By drilling down to regional and country-level data, this new Regional Risks for Doing Business report allows us to gauge how risk sentiment is evolving around the world. Cyber-attacks are increasing in prominence, but it is striking how many business leaders point to unemployment and national governance as the most pressing risks for doing business in their countries,” said Aengus Collins, Head of Global Risks and the Geopolitical Agenda at the World Economic Forum.

“Cyber-attacks are seen as the number one risk for doing business in markets that account for 50% of global GDP. This strongly suggests that governments and businesses need to strengthen cyber security and resilience in order to maintain confidence in a highly connected digital economy,” said Lori Bailey, Global Head of Cyber Risk, Zurich Insurance Group, and Member of the Forum’s Global Future Council on Cybersecurity.

“While large cyber-attacks are the number one concern of executives in advanced economies there is growing apprehension about the potential for national governance failures in emerging markets,” said John Drzik, President of Global Risk and Digital at Marsh. “Across the globe, businesses are also concerned with rising geopolitical friction that has already resulted in rising tariffs and sanctions and which could further fuel the growing threat of expropriation or political violence.”

Top five risks of doing business by region

Methodology

The findings of the Regional Risks for Doing Business report are based on 12,548 responses from executives in 140 economies. Respondents were asked to select “the five global risks that you believe to be of most concern for doing business in your country within the next 10 years”. This question is included in the annual Executive Opinion Survey, which is a part of the World Economic Forum’s Global Competitiveness Report. The latest edition of the survey was carried out from January to June 2018. Business leaders were asked to choose up to five risks from a list of 30, including terrorist attacks, extreme weather events and state collapse or crisis.