Authors: Tim Gould & Ali Al-Saffar*

The pitfalls of relying on oil and gas revenues to fuel an entire economy have long been recognised: strategies aimed at economic diversification have featured in national development plans of major hydrocarbon-exporting economies since the early 1970s.

But the fall in oil prices that began in 2014 has given this debate a new urgency. It provided a reminder of the damage that the downswing in a commodity cycle can bring, with non-hydrocarbons sectors bearing the brunt of the decline in revenues. It also raised further questions about the long-term structural implications of two ‘revolutions’ in the world of energy: shale as a new source of supply, and the gathering implications of clean energy transitions on the demand side, including improvements in fuel efficiency and the rise of electricity as an alternative to oil in parts of the transportation sector.

In a new report, the Outlook for Producer Economies, we examine what these structural changes might mean, in different scenarios, for a diverse group of the world’s leading oil and gas exporters: Iraq, Nigeria, Russia, Saudi Arabia, the United Arab Emirates and Venezuela.

Stay ahead of the geopolitical week.

MD Briefing delivers expert analysis across five global fronts — the Indo-Pacific, energy, geoeconomics, European security, and the Middle East — every Monday morning. Free.

The results underline the strategic importance of the reform initiatives that are underway in many of these countries. Economic transformation and diversified growth are essential not only to deal with the changing dynamics of global energy, but also to generate opportunities for growing populations, including large numbers of young people entering the workforce in Iraq, Nigeria and Saudi Arabia.

Arguments for economic diversification often focus on the downside of resource abundance. There are ample reasons for concern: the volatility of oil and gas revenue – as shown above – creates public policy dilemmas for which there is no easy answer, and there are other potential pitfalls besides. But energy should not only be seen as part of the problem. In practice, our report shows that a well-functioning energy sector – bringing a wider range of resources and technologies into play – can be a durable source of advantage to today’s producers, providing some of the capital and know-how that can support more diversified growth. The reform process will be complex and challenging, but change in the energy sector is part and parcel of the development of more productive, innovative and sustainable economies.

In the Outlook for Producer Economies, we identify six areas where the outlook for the energy sector is closely tied to the broader reform agenda:

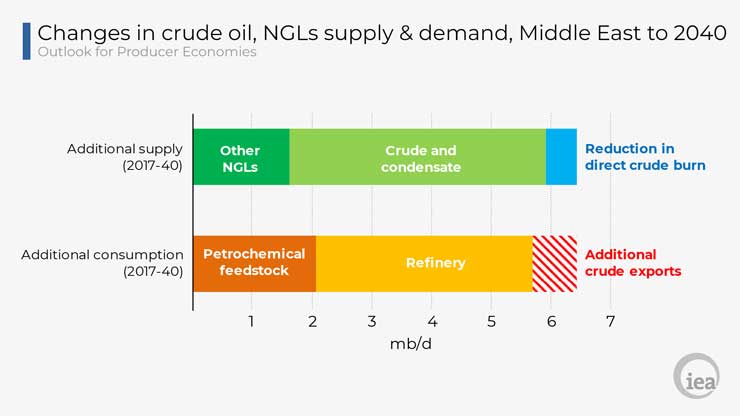

Capturing more domestic value from hydrocarbons: Many producers, including those in the Gulf and in Russia, are moving downstream in order to capture additional value from hydrocarbons resources, often co-locating new petrochemical facilities with refineries to capture operational synergies. Expansion into petrochemicals offers the potential for more resilient margins. Demand for petrochemical products, even with growing attention to reducing single-use plastics and increasing recycling, is relatively robust across different energy scenarios. Since they are not combusted, there are no direct emissions associated with the use of oil or gas as petrochemical feedstocks. In our main scenario, the Middle East remains by far the largest global oil exporter, but almost all of the increase in oil production in the Middle East to 2040 goes into refining or petrochemicals.

Use natural gas strategically in support of diversification goals: Natural gas has been a junior partner to oil in many producer economies, less lucrative and often produced as a by-product of oil developments as associated gas. But the potential significance of natural gas for diversification strategies is larger: it displaces oil in many applications and can also underpin an industrial strategy in a way that oil cannot. There is a need for strategic calculation about where and how gas – often together with renewables – can bring the best value to the energy system. Infrastructure is still lacking in some instances: Iraq and Nigeria still flare significant volumes of gas despite domestic shortages of electricity. Another challenge, especially in some parts of the Gulf, is to adapt pricing policies so that operators seek and produce gas as a commodity in its own right.

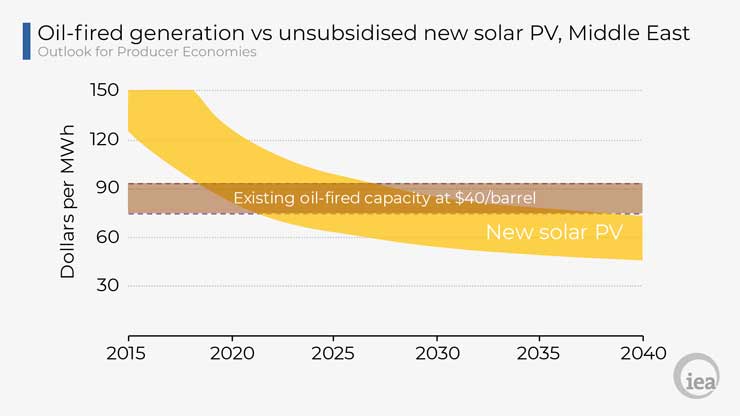

Tap the huge, under-utilised potential of renewables: Demand for electricity is growing fast across the Middle East and almost all of this increase has been met by gas-fired and oil-fired plants, despite the plummeting cost of new renewables-based electricity. Investment activity has picked up, but solar PV still makes up less than 1% of total generation in the Middle East; the opportunity cost of burning around 1.8 mb/d of oil to provide electricity is especially significant at a moment when global spare production capacity is starting to look thin. Even If oil were priced for generation at $40/barrel (well below its current market value), unsubsidised solar would be displacing it quickly. Solar resources are abundant and are also ideally suited to meeting the peak in the region’s summer generation due to air conditioners: in Saudi Arabia, daily demand for cooling peaks in the early afternoon and is a good match with peak solar PV output.

Phase out subsidised consumption of fossil fuels: pricing reforms have gained momentum in recent years, but the continued availability of oil products and natural gas at artificially low prices encourages wasteful consumption and distorts broader investment incentives across the economy. Even without subsidies, oil and gas exporters would still have a comparative advantage in energy, since a low production cost base can provide a stable low domestic price. This is of particular value in the case of gas and electricity, where a global commodity market is constrained by infrastructure bottlenecks and high transport costs, or does not exist at all. The report outlines how the implications of pricing reform for energy consumers can be mitigated substantially if reform is paired with enhanced energy efficiency measures, with significant fiscal and environmental benefits.

Ensure adequate investment in the upstream: The ability to maintain oil and gas revenues at reasonable levels provides an important element of stability for the economy as a whole, especially when market conditions are tough. It is therefore crucial for producers to maintain flows of investment to the upstream, even as they seek to broaden investment flows across their economies. Venezuela provides a stark example of the risks; a collapse in upstream spending has exacerbated shortfalls in revenue and accelerated the downward spiral of the economy as a whole.

Support the development of cleaner and more efficient energy technologies: Many producers have world-leading expertise in energy technologies; in addition to their potential in renewables, they are also well-positioned to develop new approaches that reduce or minimise the lifecycle emissions of oil and gas. Saudi Arabia and the United Arab Emirates, for example, are scaling up interest in carbon capture, utilisation and storage. Oman is pioneering the use of large concentrating solar projects for enhanced oil recovery. There are large-scale opportunities to pair up solar energy with the Middle East’s demand for desalination and clean water. It should not be taken for granted that the comparative advantage in energy of major producers diminishes in the energy transitions.

*Ali Al-Saffar, Energy Analyst.