Distributed ledger technologies (DLT) – of which blockchain is the best known form – could play a major role in reducing the worldwide trade finance gap, enabling trade that otherwise could not take place, finds a new study by the World Economic Forum and Bain & Company. Its effects would be largest in emerging markets and for small and medium-sized enterprises (SMEs), showing the use of the technology beyond large corporations and developed markets.

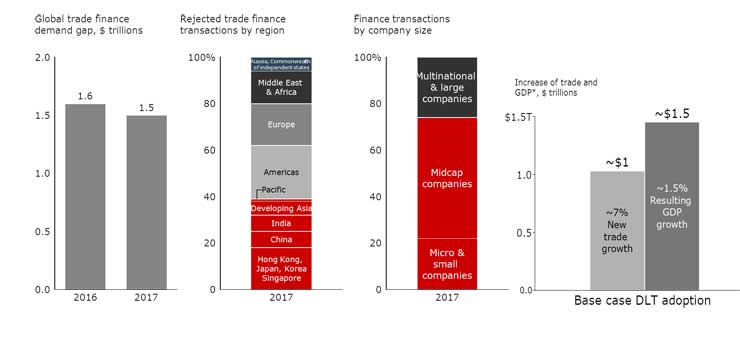

The global trade finance gap currently stands at $1.5 trillion, or 10% of merchandise trade volume, and is set to grow to $2.4 trillion by 2025, the Asian Development Bank calculates. But a new study shows that this gap could be reduced by $1 trillion if DLT is used more broadly. The largest opportunities could come from smart contracts, single digital records for customs clearance. They would help mitigate credit risk, lower fees and remove barriers to trade.

If implemented, the main beneficiaries are set to be SMEs and emerging markets, which suffer most from a lack of access to credit and have ample room to grow trade. “Implementing blockchain-based solutions can eventually do more for SMEs in emerging markets than removing tariffs or closing trade deals,” said Wolfgang Lehmacher, Head of Supply Chain and Transport Industry at the World Economic Forum.

The trade financing issue, and the proposed DLT solution, are particularly important for Asian economies, including ASEAN, China and Hong Kong SAR, India and Korea. They account for almost three-quarters of total documentary for import-export transactions, and account for almost 7% (or $105 billion) of the trade finance gap. But for countries to benefit, they will need a coordinated approach.

Stay ahead of the geopolitical week.

MD Briefing delivers expert analysis across five global fronts — the Indo-Pacific, energy, geoeconomics, European security, and the Middle East — every Monday morning. Free.

“The benefits of adopting DLT in trade will affect everyone from banks to companies to governments to consumers,” said Gerry Mattios, Expert Vice-President at Bain & Company, and a key contributor to the study. “But action has to be taken in a collaborative way and with an ecosystem approach in mind. Individual actions won’t bring the expected results.”

If the recommendations are implemented and the estimated impact materializes, it would be one of the first cases where blockchain is mostly beneficial to SMEs and emerging markets, as opposed to large banks or technology companies in developed markets.