Take a close look at your smart phone for a moment. What do you see? A glass screen. A button equipped with fingerprint recognition. A camera lens, flashlight, microphone, and speaker. Each of these components, and others – including chips, processors, batteries – are independently sourced from companies located all over the world and assembled into a finished product at factories, often in China. Any smart phone you purchase, and its components, has likely passed through customs several times, landed on multiple countries and continents, and been touched by countless workers.

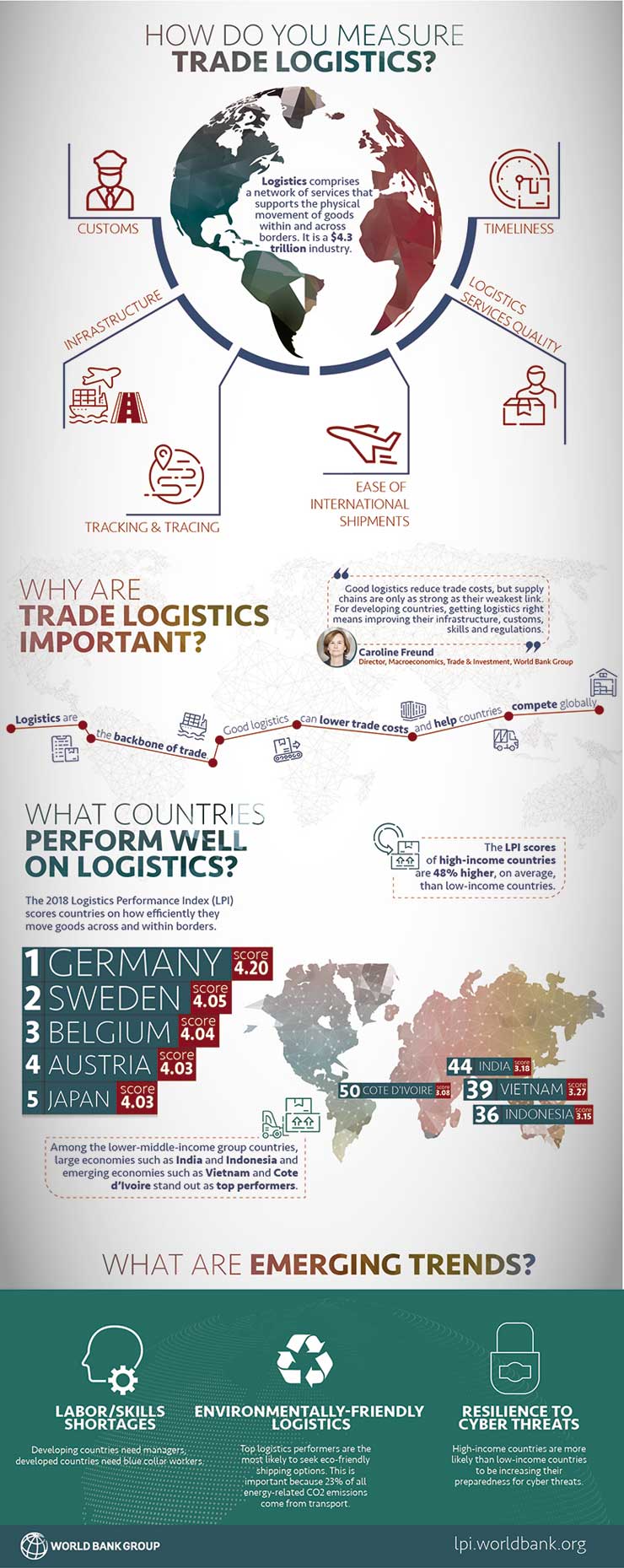

Logistics makes all this possible. A $4.3 trillion industry affecting nearly every country in the world, logistics is the network of services that supports the physical movement of goods within and across borders. It comprises an array of activities including transportation, warehousing, brokerage, express delivery, terminal operations, and even data and information management. How efficiently goods can move through these systems to their final destinations is a key determinant to a country’s trade opportunities.

“Logistics are the backbone of global trade,” notes Caroline Freund, Director, Macroeconomics, Trade & Investment Global Practice at the World Bank Group. “As supply chains become more globally dispersed, the quality of a country’s logistics services can determine whether or not it can participate in the global economy.”

Benchmarking Logistics Performance

Stay ahead of the geopolitical week.

MD Briefing delivers expert analysis across five global fronts — the Indo-Pacific, energy, geoeconomics, European security, and the Middle East — every Monday morning. Free.

With trade and logistics touching so many areas of an economy, it can be difficult to get a complete picture of a country’s performance. This is why the Logistics Performance Index (LPI), part of the biennial report Connecting to Compete, evaluates countries across a number of indicators. The index, which takes into account factors such as including logistics competence and skills, the quality of trade-related infrastructure, the price of international shipments, and the frequency with which shipments reach their destination on time, helps governments benchmark their progress over time and in comparison to similar countries.

Utilizing surveys of logistics professionals, the LPI offers two perspectives on a country’s performance:

The domestic LPI offers quantitative and qualitative assessments of a country’s services from logistics professionals working inside the country. This component offers detailed information on a country’s infrastructure, quality of service providers, border procedures, and supply chain reliability.

The international LPI provides evaluations of a country’s services by logistics professionals located outside the country. This component provides qualitative information of how a country’s trading partners perceive the efficiency and quality of its logistics services.

The World Bank Group has been scoring countries on these issues every two years since the inaugural edition of Connecting to Compete in 2007. Consistently, high-income countries, particularly those in Western Europe, emerge as world leaders on logistics. In fact, the LPI score of high-income countries is 48% higher, on average, than low-income countries. Among the 30 top performing countries, 24 are members of the Organization for Economic Co-operation and Development (OECD).

“Across the board, we have seen most countries investing in logistics-related reforms, especially in the areas of building infrastructure and facilitating trade,” explains Jean Francois-Arvis, Economist at the World Bank Group and report co-author. “Despite these efforts to modernize services, developing countries face many remaining challenges. This explains a persistent gap between high- and low-income countries in terms of logistics performance.”

But income alone is not the sole determinant of a country’s LPI score. Vietnam, Thailand, Rwanda, China and India all outperform their income groups. These countries tend to have access to sea ports or large international transportation hubs.

For individual countries, logistics performance is key to their economic growth and competitiveness. Inefficient logistics raise the cost of doing business and reduce the potential for integration with global value chains. The toll can be particularly heavy for developing countries trying to compete in the global marketplace. Governments can use the LPI to better understand the link between logistics, trade, and growth, and what policies they can enact to globally compete.

2018 LPI: Key Findings

The top 10 performing countries have remained relatively unchanged over the past few years and tend to include high-income countries in Europe. Of the top 30 performers, 24 are members of the OECD.

The bottom 10 countries in the ranking are composed of mostly low-income and lower-middle-income countries. These are either fragile economies affected by armed conflict, natural disasters, political unrest, or landlocked countries that are naturally challenged by geography or economies of scale in connecting to global supply chains.

The LPI scores of high-income countries, on average, surpass low-income countries by 48 percent.

Among the lower-middle-income group countries, large economies such as India and Indonesia and emerging economies such as Vietnam and Cote d’Ivoire stand out as top performers. Most of these countries either have access to the sea or are located close to major transportation hubs.

There is currently a labor shortage of logistics professionals in both developed and developing countries. Developed countries need more blue-collar workers, such as truck drivers, while developing countries seek more managerial-level workers.

More countries perceive cybersecurity threats a risk to logistics. However, while 78% of high-income countries have increased their preparedness, only 26% of low-income countries have done so.

Given that 23% of all energy-related CO2 emissions can be attributed to transport, the environmental sustainability of logistics is an important emerging trend. Strong performers in logistics are the most likely to seek eco-friendly shipping options. In the top quintile of LPI performers, 28% of respondents indicated that shippers often or nearly always ask for environmentally friendly shipping options. In the bottom quintile, this percentage falls to just 5%.