The growth of oil production from the United States has led to fundamental changes in global oil markets in recent years. Thanks to the shale revolution, the United States is becoming the world’s top oil producer. Growth is led by shale production from the Permian Basin, where output is expected to double within the next five years.

But with this surge, a question is whether this extra oil from the United States is the right kind for global markets and refiners.

To answer, it is useful to take a short detour in refining operations. Nearly every barrel of oil must be refined into a range of products to satisfy different markets and uses. But crude oil comes in different flavours (sweet, or low-sulphur, and sour, or high-sulphur) and weight classes (heavy, medium, light and ultralight.) These two measures of quality – sulphur content and density – are the most important factors when refiners select types of crude oil to process. Refineries have to remove close to 80% of the naturally incurring sulphur in crude oil through energy-intensive processing. Low-sulphur crude oils generally carry a premium over high-sulphur crudes.

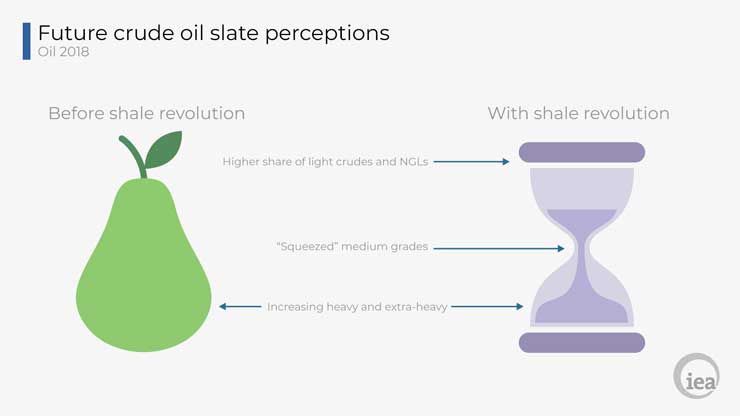

Density, on the other hand, does not have such linear relationship with price. Light oil can be turned into gasoline more easily than heavy grades, while medium gravity grades produce more diesel and kerosene, fuels used in road transport and aviation. Heavy crudes yield too much atmospheric residue that cannot be monetised profitably. Adjusting refining processes to the type of crude oil being refined is therefore critical to maximize refining output and profits. Before the US shale revolution, refiners around the world had been gearing up for a world of heavier crudes by investing in so-called deep conversion units needed to process heavy oil into gasoline and diesel. Most of the growth in crude oil production was concentrated in heavy barrels, such as Canadian oil sands. In this view, the future crude-oil mix would be pear-shaped, with heavy-grade at the bottom of the barrels accounting for a growing share of the total.

Stay ahead of the geopolitical week.

MD Briefing delivers expert analysis across five global fronts — the Indo-Pacific, energy, geoeconomics, European security, and the Middle East — every Monday morning. Free.

But the growth of US light oil from shale is changing this view to an hour-glass shape, where the proportion of light and heavy barrels compared with conventional medium-heavy grades increases. The return of OPEC’s market management with Russian cooperation adds to this view since, together, OPEC producers and Russia account for three quarters of the world’s medium-grade barrels.

During the first wave of shale development, when crude exports were not allowed (except shipments to Canada) the US refining system was able to absorb most of the LTO volumes. Between 2010 and 2015, shale output grew by 3.8 mb/d. Imports of light African oil decreased, some 500 kb/d of distillation or condensate splitting capacity was built to allow refineries to process the lower-priced LTO. Refiners preferred cheaper domestic oil even if this lead to underutilisation of their conversion capacity that was geared to processing heavier crude oil. Past investments into cokers, hydrocrackers and other conversion units are sunk costs, which are not taken into account in day-to-day feedstock selection models that refiners run to define optimal combinations of crude supply and product output. Market prices for crude oil and refined products are what primarily drive the choice.

The second wave of the US shale growth will bring an additional 3.3 mb/d of LTO to the markets over the next few years. With the lifting of the US ban on oil exports and with the infrastructure lining up to enable export flows, most of these extra barrels are likely to end up being exported overseas.

The question for US producers is whether there will be a mismatch between the perceived appetite for medium gravity crude by refiners globally and the growing LTO volumes?

IEA analysis shows that this will not be the case. Middle distillates have a seemingly uncontested monopoly in road freight and aviation, but these two sectors combined account for less than 20% of global oil demand. In road freight, the penetration of LNG trucks and electric buses in China shows that cracks are already appearing in the monopoly of diesel, while in the United States and Europe, the mandated biodiesel blend has quietly eaten into its share. Chinese refiners, for example, are trying to reduce diesel yields as the country’s diesel demand has slowed significantly.

It is very likely that diesel demand will be boosted again by the new regulations on bunker fuel sulphur emissions from the International Maritime Organization that will come into force in 2020. In the absence of readily available low-sulphur fuel oil, ship owners will resort to various marine gasoil blends. However, the result will be an excess of high-sulphur fuel oil. Any crude that yields higher quantities of diesel than LTO will also yield higher atmospheric residue, and is almost certain to contain more sulphur.

Refiners, especially those constrained by desulphurization capacity, will try to optimise feedstock choice, giving preference to low-sulphur and low-residue yield crude oil, not necessarily gasoil-rich crude oil. This is likely to be the case in Europe, where refiners will also face a decreasing availability of African light sweet oil in international markets. At the same time, Asia’s growing demand for chemicals has sparked a petrochemical construction boom. LTO, along with condensates, is a feedstock that is best suited for refineries with integrated petrochemical operations. Thus, most of the incremental output of US LTO is expected to eventually find home in Asian markets for petrochemical feedstocks and in European market as a low-sulphur, low residue yield feedstock.