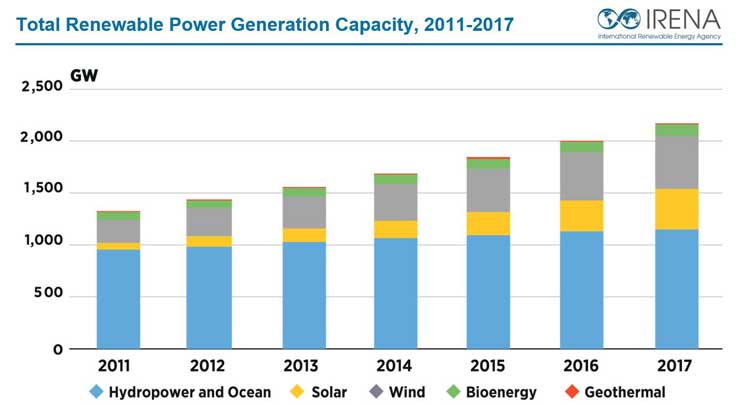

By the end of 2017, global renewable generation capacity increased by 167 GW and reached 2,179 GW worldwide. This represents a yearly growth of around 8.3%, the average for seven straight years in a row, according to new data released by the International Renewable Energy Agency (IRENA). Renewable Capacity Statistics 2018 is the most comprehensive, up-to-date and accessible figures on renewable energy capacity statistics. It contains nearly 15,000 data points from more than 200 countries and territories.

“This latest data confirms that the global energy transition continues to move forward at a fast pace, thanks to rapidly falling prices, technology improvements and an increasingly favourable policy environment, said IRENA Director-General Adnan Z. Amin. “Renewable energy is now the solution for countries looking to support economic growth and job creation, just as it is for those seeking to limit carbon emissions, expand energy access, reduce air pollution and improve energy security.”

“Despite this clear evidence of strength in the power generation sector, a complete energy transformation goes beyond electricity to include the end-use sectors of heating, cooling and transportation, where there is substantial opportunity for growth of renewables,” Mr. Amin added.

Stay ahead of the geopolitical week.

MD Briefing delivers expert analysis across five global fronts — the Indo-Pacific, energy, geoeconomics, European security, and the Middle East — every Monday morning. Free.

Solar photovoltaics (PV) grew by a whopping 32% in 2017, followed by wind energy, which grew by 10%. Underlying this growth are substantial cost reductions, with the levelised cost of electricity from solar PV decreasing by 73%, and onshore wind by nearly one-quarter, between 2010 and 2017. Both technologies are now well within the cost range of power generated by fossil fuels.

China continued to lead global capacity additions, installing nearly half of all new capacity in 2017. 10% of all new capacity additions came from India, mostly in solar and wind. Asia accounted for 64% of new capacity additions in 2017, up from 58% last year. Europe added 24 GW of new capacity in 2017, followed by North America with 16 GW. Brazil set itself on a path of accelerated renewables deployment, installing 1 GW of solar generation, a ten-fold increase from the previous year.

Off-grid renewables capacity saw unprecedented growth in 2017, with an estimated 6.6 GW serving off-grid customers. This represents a 10% growth from last year, with around 146 million people now using off-grid renewables.

Highlights by technology:

Hydropower: The amount of new hydro capacity commissioned in 2017 was the lowest seen in the last decade. Brazil and China continued to account for most of this expansion (12.4 GW or 60% of all new capacity). Hydro capacity also increased by more than 1 GW in Angola and India.

Wind energy: Three-quarters of new wind energy capacity was installed in five countries: China (15 GW); USA (6 GW); Germany (6 GW); UK (4 GW); and India (4 GW). Brazil and France also installed more than 1 GW.

Bioenergy: Asia continued to account for most of the increase in bioenergy capacity, with increases of 2.1 GW in China, 510 MW in India and 430MW in Thailand. Bioenergy capacity also increased in Europe (1.0 GW) and South America (0.5 GW), but the increase in South America was relatively low compared to previous years.

Solar energy: Asia continued to dominate the global solar capacity expansion, with a 72 GW increase. Three countries accounted for most of this growth, with increases of 53 GW (+68%) in China, 9.6 GW (+100%) in India and 7 GW (+17%) in Japan. China alone accounted for more than half of all new solar capacity installed in 2017. Other countries that installed more than 1 GW of solar in 2017 included: USA (8.2 GW); Turkey (2.6 GW); Germany (1.7 GW); Australia (1.2 GW); South Korea (1.1 GW); and Brazil (1 GW).

Geothermal energy: Geothermal power capacity increased by 644 MW in 2017, with major expansions in Indonesia (306 MW) and Turkey (243 MW). Turkey passed the level of 1 GW geothermal capacity at the year-end and Indonesia is fast approaching 2 GW.